Welcome to Machina Capitalis, my personal one-man hedge fund and the sister publication to The Royalty King. Here I detail the mechanics of running a one-man book using options, mostly for income — borderless cash flow has always been the objective.

In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

Today I want to talk about what is probably the most overrated options strategy there is: selling put options for income. You’ll have heard people spruik it. It’s not a bad strategy. But it is badly misused, and most of the people selling it to you have never actually run it. They take the idea, package it, and sell it as a newsletter — they don’t post their P&L or their trade list, which tells you everything. I’d rather show you how it works from the seat of someone who does this for a living, and let you judge the difference for yourself.

Nothing here is advice. Everything is subject to loss.

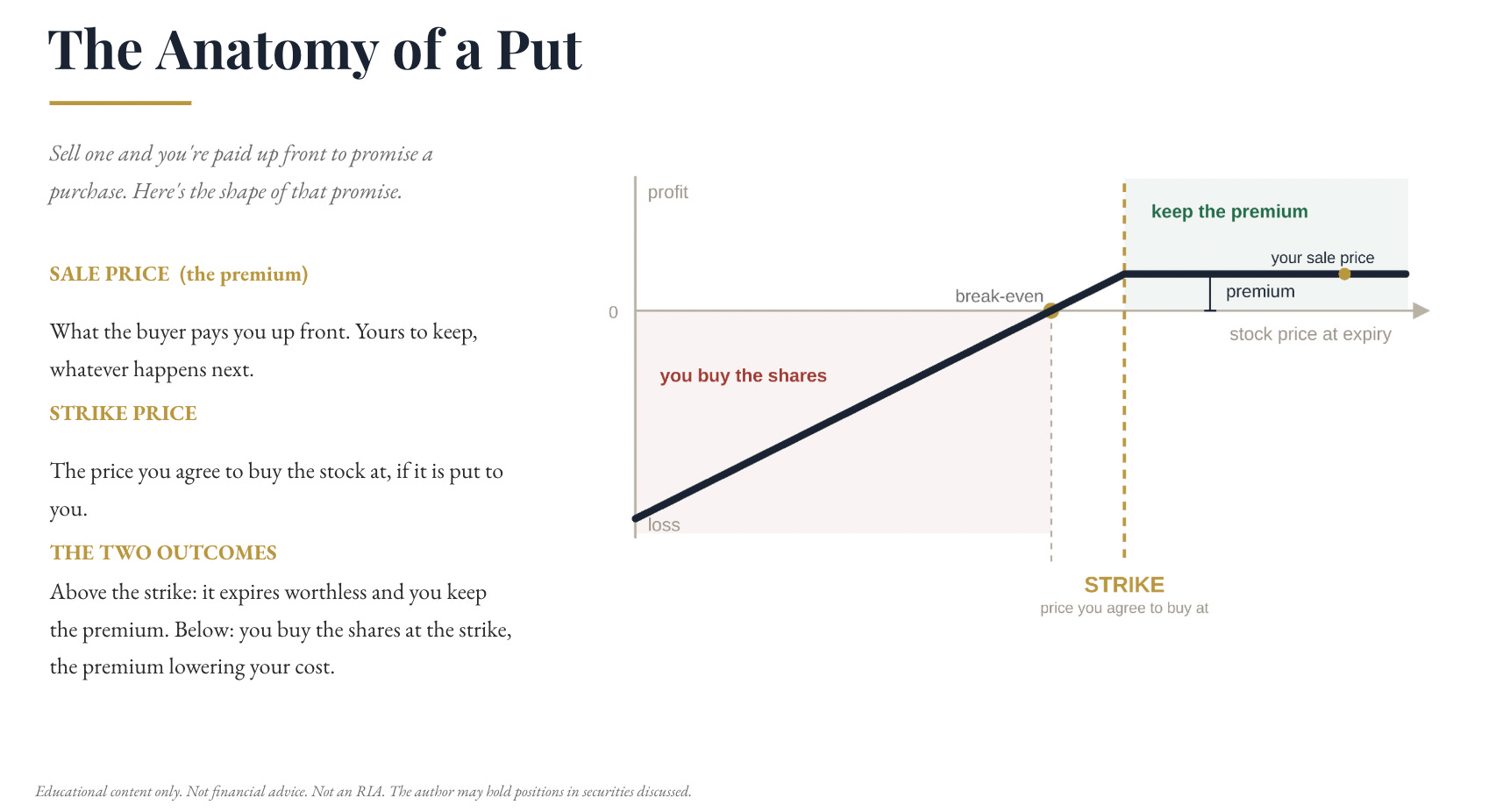

The anatomy, kept simple

There’s a stock trading at a price, and there’s a derivative market where people buy and sell the right to transact that stock at other prices on a future date.

When you sell a put, you’re making a promise: if the stock falls below your strike by expiry, you must buy 100 shares per contract at that strike — even if it goes to zero. In exchange, you’re paid a premium up front. If the stock stays above your strike, the contract expires worthless and you keep the lot. It’s a risk-transfer mechanism. You’re the insurer.

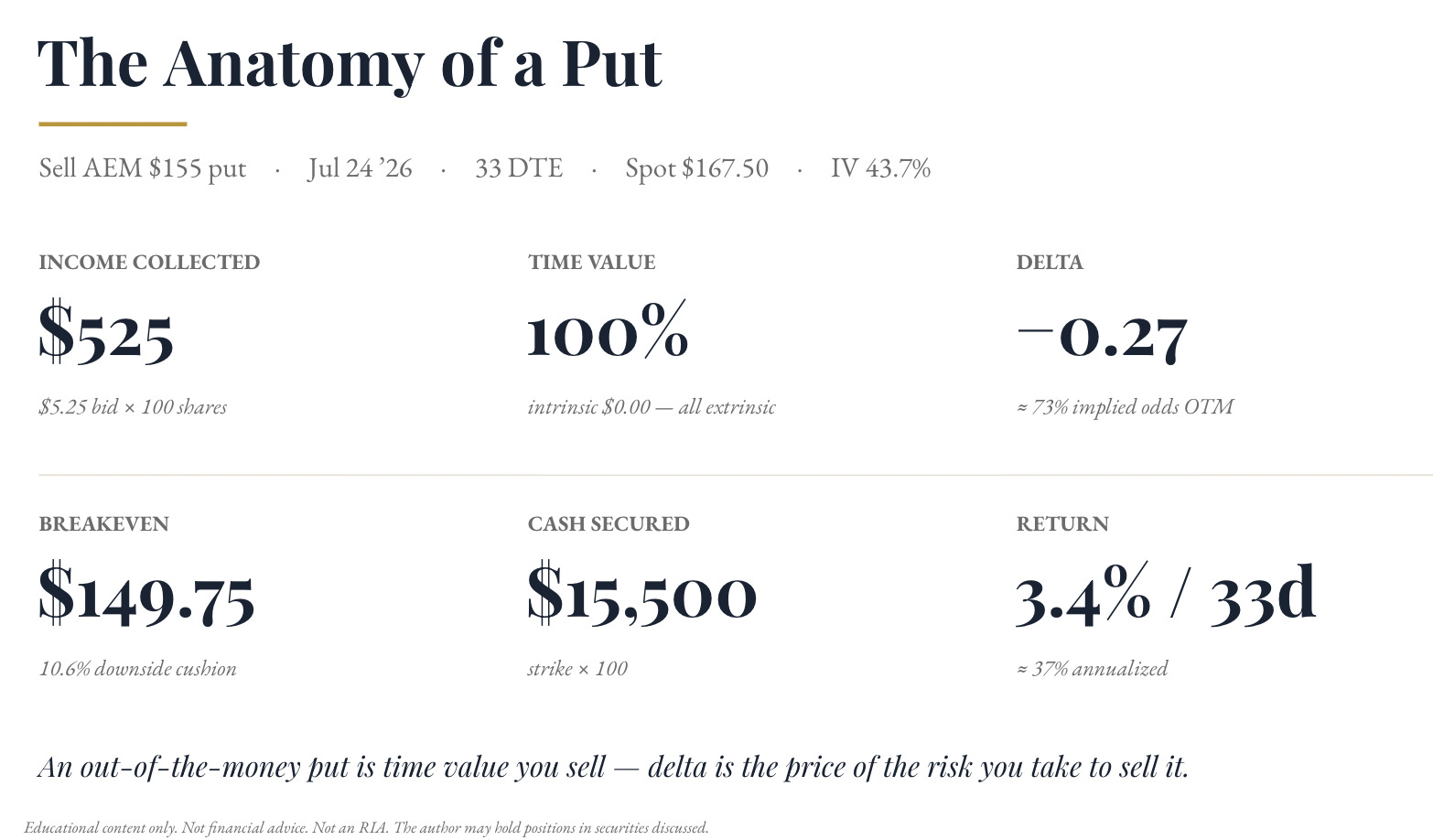

To make it concrete, I pulled up the first ticker that came to mind beginning with “A” — Agnico Eagle. Not a recommendation, I don’t own it. Say it’s trading around $166. Sell the $155 put ~33 days out and collect roughly $5.25. That’s $525 per contract. If the stock sits above $155 at expiry, you keep it: about 3.4% over 33 days, or ~33% annualised.

Sounds wonderful. And you’ll hear the pitch: “If it’s a stock you’d want to own anyway, why not get paid to wait?” There’s logic to that. The problem is the gap between that logic and a practitioner doing this repeatedly, month after month, as an actual income source.

The “quit your job” math

Let’s say someone wants to replace their wage with this. US median wage is about $63,300 a year. At that rate of return you’d need roughly $169,000 of working capital and you’d have to roll about 11 puts a year to pull ~$5.8K a month.

It’s just not realistic to expect that. The trade doesn’t always go your way — you’ll get assigned, you’ll have to buy shares, and that chews working capital. Spreading across enough positions to avoid single-name risk, being right month in and month out — I’ve never seen anyone do it on this tactic alone. Use margin to juice it and you invite the other failure mode: the broker stops you out on their timing, not yours, crystallising losses to keep your equity-to-margin balance in line.

It feels like free money until it doesn’t. Eleven good months and then month twelve hands you an event — stock-specific or market-wide — that sells the position down for more than the premium you banked all year. Your upside was capped at the premium the whole time; your capital was locked the whole time. If a better opportunity showed up mid-stream, you couldn’t always free yourself to take it without booking a loss.

Two philosophies

The Croupier. Sell monthly, close to the money, harvest the most time value. Plan your loss in advance — maybe twice the premium — and if it draws down to there, you close and move on. If it works, you buy back early at ~70% of the profit within a week or two and roll into the next setup. It works on paper. In practice it’s a lot of management, and you have to be right far more often than is realistic. I genuinely don’t know anyone who runs this in isolation and wins consistently.

The insurance writer. This is the Buffett-style version, and the one I actually prefer. The trick is to move out in time — six to twelve months or longer — and down in strike, to a 15–20 delta well below spot. You’re not gambling on next month’s noise. You’re getting paid a reasonable premium to wait to buy something you’d be thrilled to own at a deep discount.

A real trade

Earlier this year I had a name trading around $76. Rather than play the short game, I looked out roughly ten months — about 312 days to expiry — and laddered in. One leg: I sold the $40 put. The premium worked out to a ~12% yield, ~14% annualised if held to expiry.

Why I like it: the stock would have to nearly halve before I’m assigned — and I’d be ecstatic to add at $40. Better still, my true break-even isn’t $40, it’s the strike minus the premium, around $35.20. Factor in the ~4.3% I’m earning on the cash balance at Interactive Brokers and the effective yield nudges toward 18–19%, depending on your bracket and whether you run cash or margin. I left that out of the headline number to keep it clean.

That’s the whole point of the long-dated, low-delta approach: I don’t need the cash sitting there to cover every trade the day I enter it. It sits as a form of leverage on the book. I’ve got a long runway to adjust — roll it, cover it by peeling cash from elsewhere, or close it out for a profit. With Agnico, by contrast, a 5% move and you’re assigned, because you’re playing the short game and praying you can roll.

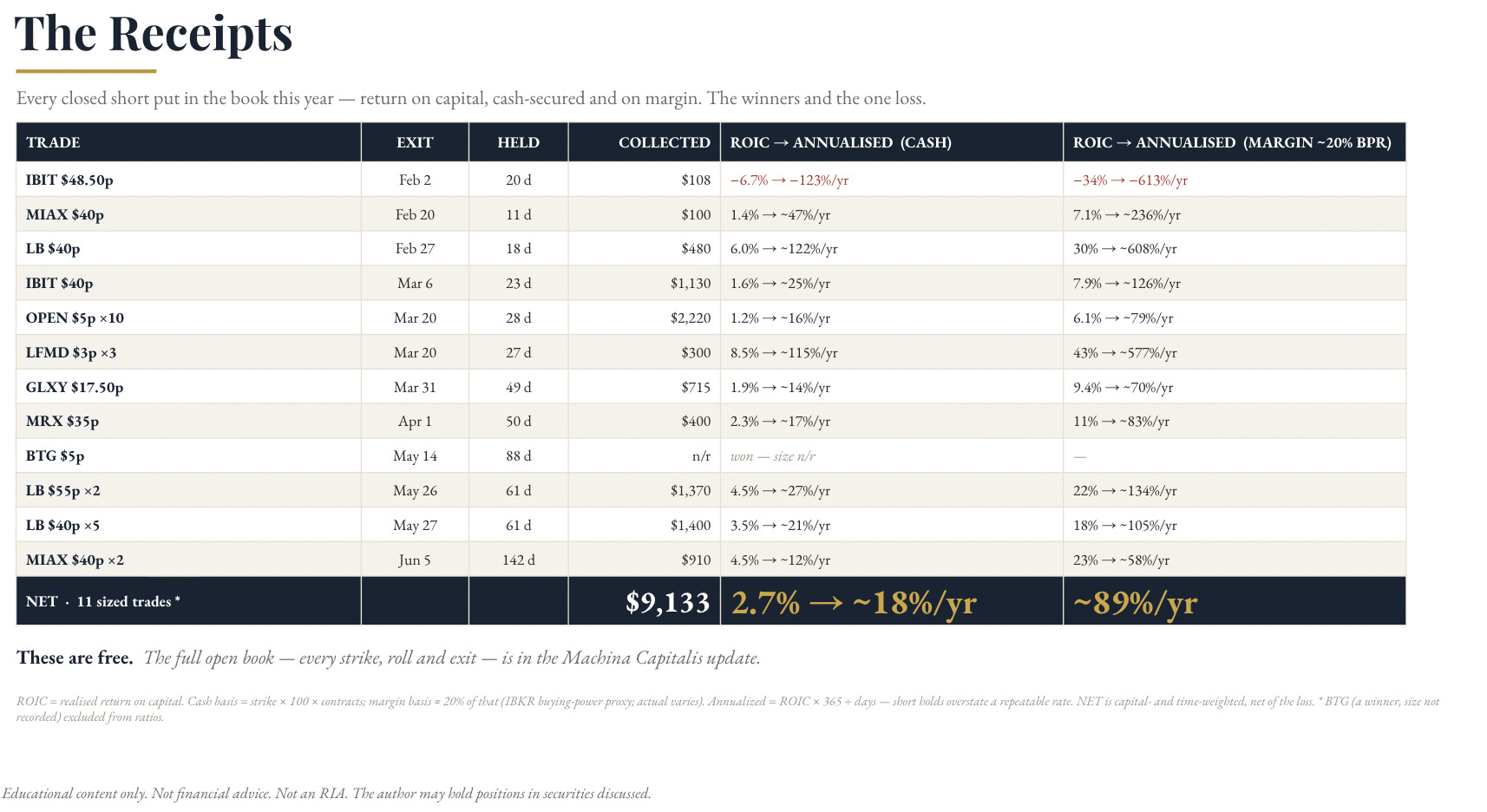

Year-to-date, my closed short-puts have run at roughly 18% on a full-cash basis — call it ~22% once you add interest. For me, this sits as leverage on the working capital in play in the options book as I don’t need to physically put cash in the deal unless I run these to assignment. As a rough rule of thumb, I like to have the collateral 20% covered which takes the ROI effectively to 89%.

And here’s the part that surprises people: this is the tactic I use least. Not because it’s bad, but because I’ve evolved my process. It’s not time-intensive, it gives me a long runway, and it sits as cheap leverage while I wait for valuations to come to me. Many of these I’ve already bought back inside two months because the profit was there. (There’s one loss in the book too — an IBIT trade where I made a mistake. The good, the bad, and the ugly all get logged.)

So: put selling ain’t put selling. Understand what you’re actually trying to accomplish, and whether one particular tactic will deliver it — consistently and realistically, not just in theory. I’m no theoretician. This is just a practitioner putting real results on the table so you can judge for yourself.

Every trade, every line — capital received, capital deployed, wins and losses — is logged for premium members at Machina Capitalis.

Remember - it ain’t easy. Anyone who says otherwise isn’t really practicing what they preach.

I’ll catch you in the next one. Take care.

Benjamin

Disclaimer: Nothing in this piece is financial advice. I am not your advisor. Everything discussed is subject to loss, including total loss of capital. Options carry significant risk and are not suitable for all investors. Past performance is not indicative of future results. Do your own research and consult a licensed professional before acting.