I Run a One-Man Hedge Fund

No investors, no office, no payroll — just capital, a handful of option structures, and an old idea of Ed Thorp's. Here is the whole system, the live trades, and — for members — the exact orders I'm placing this week.

There is a particular kind of freedom in answering to no one.

I don’t run a hedge fund in the regulatory sense; there are no limited partners, no capital calls, no quarterly letter I owe to anyone but myself and the readers who choose to look over my shoulder. It is a book of my own capital, operated from wherever I happen to be standing, built for a single purpose: to generate cash flow that does not depend on a post code.

So why would anyone want to do that? Because the alternative, for me, had stopped making sense. I came out of COVID having spent years building private businesses and rolling them up, and the world I returned to was not the one I had left. The effort-to-reward had quietly inverted. More to the point, none of it travelled. You cannot fold a service business into a carry-on. You cannot take real estate through customs. I wanted the thing that an in-person enterprise can never give you — the ability to deploy capital, and harvest income from it, from anywhere — and I set about building it deliberately. The first sketches of this idea were drawn in Panama in 2023. This publication is the documentation of where they led.

A necessary word before any of the rest. Nothing here is advice. I share only real trades I have on or am putting on, alongside the occasional theoretical deployment, for the record. Past performance guarantees nothing. There is no guarantee of any performance whatsoever. This is a journal, not a tip sheet.

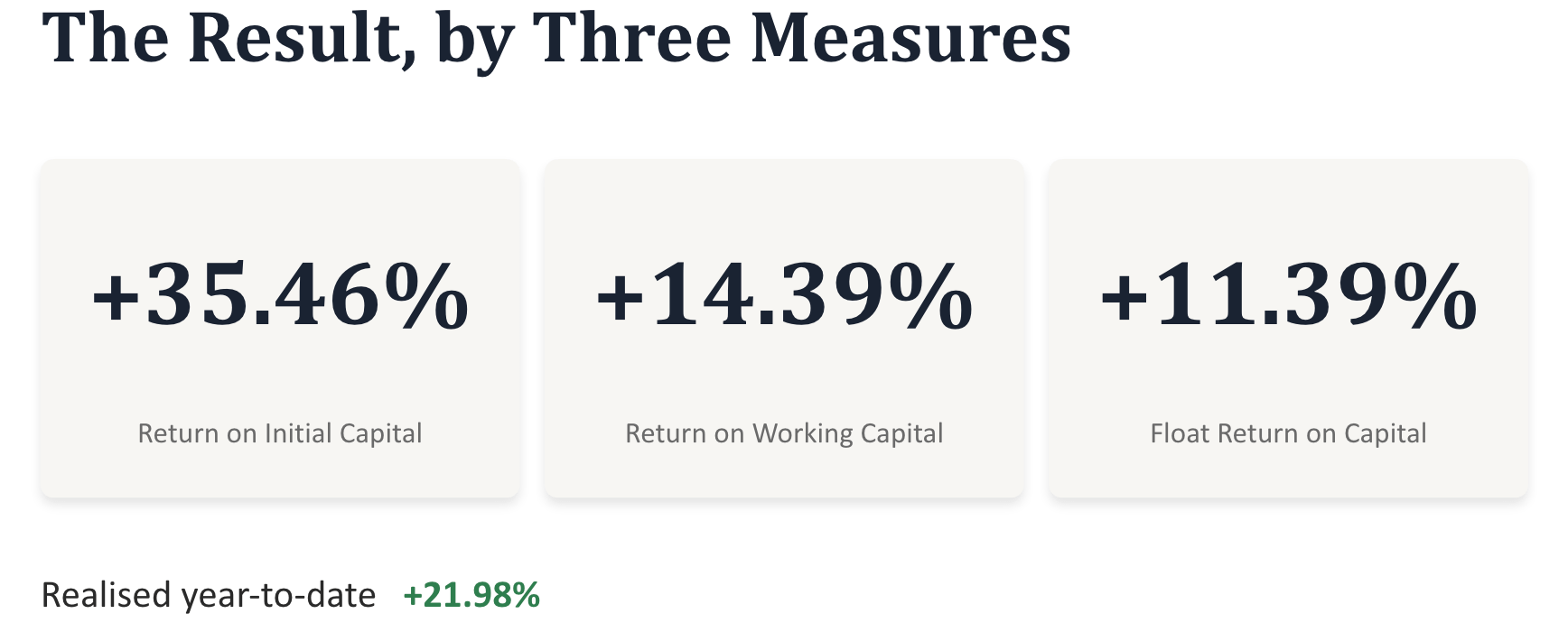

Where the book stands

Year-to-date, the number that matters most to me is twenty-two percent — those are the realised gains in 6 months. Realised = banked, already accounted for. Not a mark, not a hope: cash. That comfortably covers the income the book is supposed to throw off, and it leaves a discussion for another day about the returns on the capital I actually put down versus the capital I get to use.

That distinction is the whole game. An insurance company makes its money on the float — on money that is not, strictly speaking, theirs. I have no desire to run a property-and-casualty insurer. I have every desire to borrow its philosophy and apply it to the one asset class most people refuse to treat as an asset class at all: leverage itself, handled with respect.

The engine is sixty years old

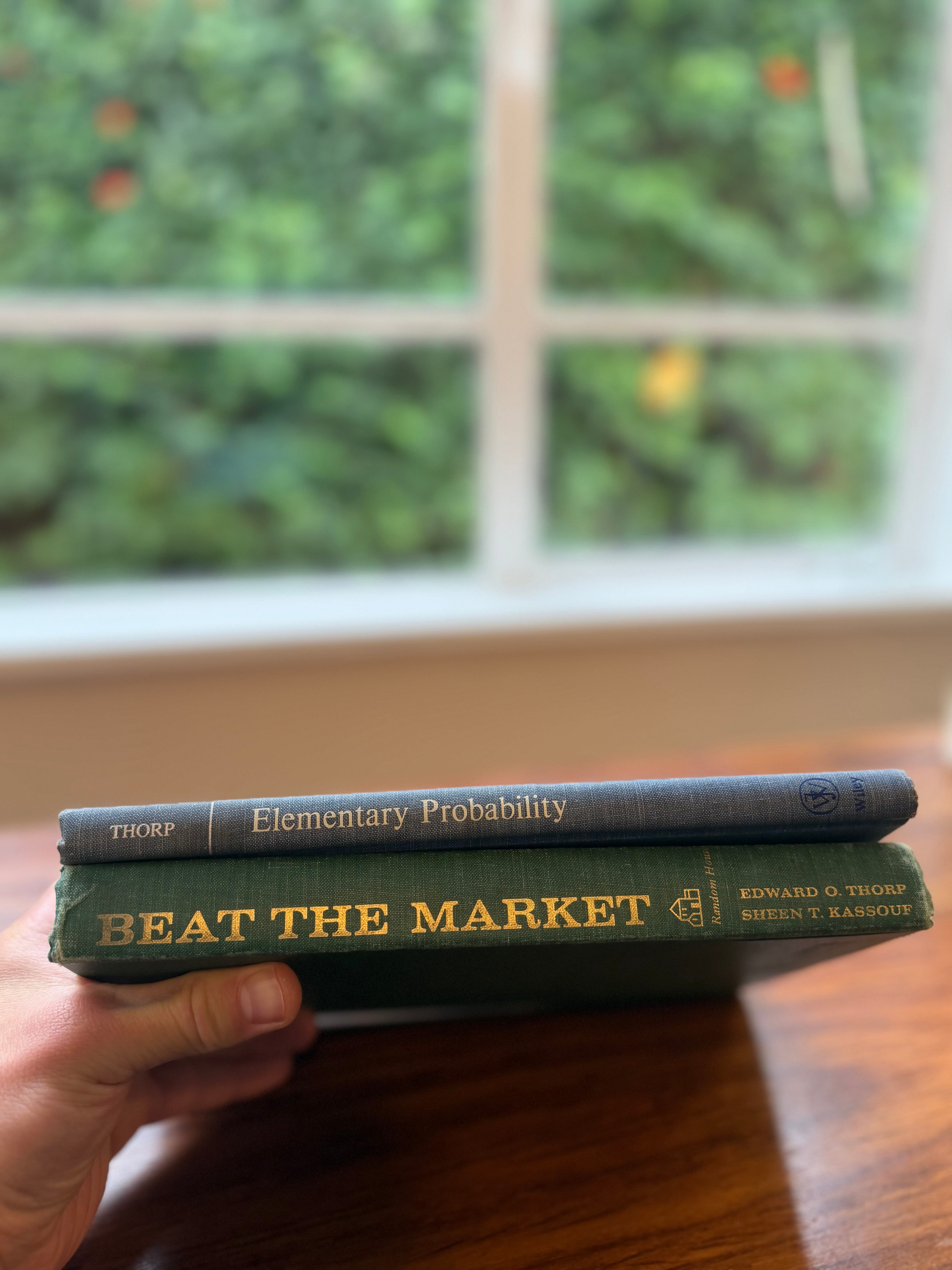

Keeping it as simple as I can, the core of what I do is an adaptation of Ed Thorp’s warrant-hedging system. If you’ve read Beat the Market — I keep a first edition — you’ll know the shape of it. Thorp used the mathematical relationship between a warrant and its underlying stock to construct positions that locked in something close to a guaranteed profit; market-neutral, indifferent to whether the index went up or down. It worked beautifully through the 1970s, a decade in which the stock market did poorly and inflation did as it pleased.

I believe that past may be somewhat prologue. So I have spent a long time sitting with Thorp’s original idea and asking how a single operator, today, with a modern options chain instead of a warrant book, might express the same thing. The answer is Machina Capitalis — a capital machine, rebuilt out of option structures.

3 Very Important Tactics

There are six structures I run. The three that carry the weight are the hedged longs — which is a dignified way of saying deep in-the-money covered calls, or buy-writes.

The mechanics are unglamorous, which is precisely the point. I own an asset I want to own. I write a call against it, lately quite deep in the money. In exchange I receive a fat premium that gives me a built-in downside cushion and a defined, knowable maximum upside. I can set the trade for six months, twelve, sometimes twenty-four. I know my worst case and my best case the day I enter. I have come, over time, to prefer this kind of elegant simplicity to almost anything else — because it is operationally efficient, and because, when done with patience it pays twenty, twenty-five, thirty percent implied returns simply for entering. You get paid to show up. This is my version of Thorp’s basic system.

It’s not as easy as it sounds - I need to adjust the ratio of long:short exposure as the trade unfolds if I wish to remain delta-neutral.

The second structure is the cash-secured put, and I do it the unfashionable way. I sell a long-dated, out-of-the-money put on a name I would be glad to own, collect the premium up front, and take the stock at a discount only if it ever reaches my strike. I do not sell weekly puts and roll them month over month. That sounds wonderful in a thread and works for almost no one over a full cycle. Recently I closed some Fermi puts I’d sold fifty-nine days earlier — for roughly 10% profit booked, which annualises near sixty. It does not always go that way. But selling insurance, long-dated and out of the money, contributes quietly and durably; the zero-day-to-expiration circus is fraught with peril.

The third is the leverage dial — the synthetic, or poor man’s, covered call. Instead of buying the stock outright and writing against it, I buy a deep in-the-money LEAP, the modern descendant of Thorp’s warrant, for a fraction of the capital, and sell a nearer-dated call against that. Same exposure as the basic system, more moving parts, a sliver of the cash. When it works the return on invested capital is something to behold. But leverage cuts both ways, and this is not a thing to pick up and start doing on any given Sunday.

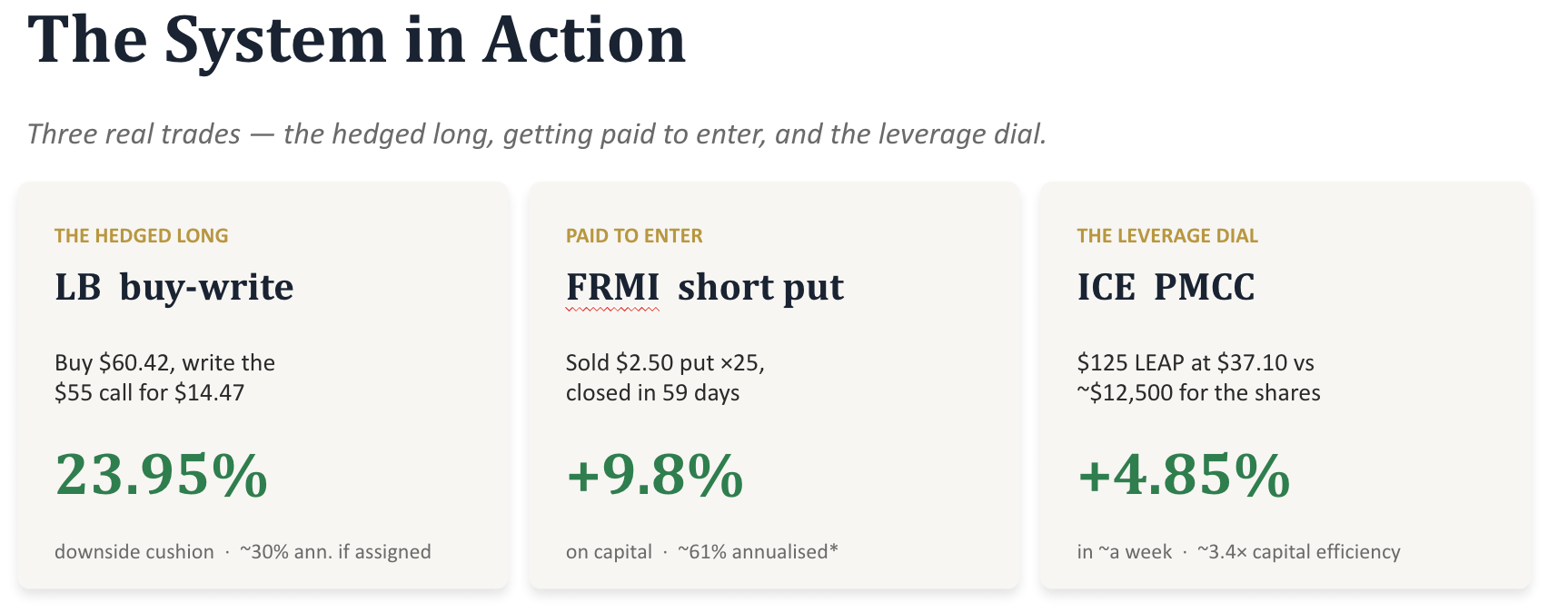

The system in action

I am a practitioner, not a theorist, and the internet is full of theorists. So, three real trades then.

The basic system: a LandBridge buy-write. I bought the stock around $60.42 and wrote an in-the-money call at $55, for which I was paid $14.47. That locks in roughly thirty percent annualised if I’m assigned, with a twenty-four percent cushion — the stock has to fall almost a quarter before I lose a dollar. Upside is capped, but that’s the concern of the long term investment portfolios covered in The Royalty King, not an operating business.

The short put: the Fermi position above. A $2.50 strike sold into a stock trading near $5, when the volatility premium was, frankly, absurd. Ten percent returned in fifty-nine days, closed.

The leverage dial: a synthetic covered call where, rather than pay $12,500 to control a hundred shares of a $125 stock, I controlled the same notional for $3,710, sold a call just out of the money against it, and closed both legs a week later for roughly 4.85% on the capital committed. A week. That is the upside of leverage.

How Much Is Needed For Freedom? A $100K Prototype.

Before scaling anything, I ask a small question: what can a single $100,000 of working capital reasonably underwrite, and does it move the needle? If I can earn thirty percent annualised (22% so far in 2026) on $100k, that’s $30,000 and approximately equal to the median annual wage in Europe. Set against a US median wage near $60k, it implies something quietly radical; two hundred thousand dollars of working capital, run this way and if the performance holds, equals/replaces a median income. No guarantees attach to that sentence. But as a thought experiment, it is the entire reason I built the machine.

The free portion ends here.

Below the line, premium members of Machina Capitalis get the rest of this issue: the exact list of names I’m underwriting over the next six months, the full order entry — stock, short strike, and the asking price I’m posting the calls at — the contract counts behind each, the blended math (≈35% downside protection across the book, close to 25% over six months, ~50% annualised if the orders fill), and how I weighted it all between the names.

If you want the order book, it’s one click away. If not, I’ll catch you in the next issue.