In Proud partnership with The Solstice Laboratory — the physics of markets, quantified. Read The Entropy Trap to discover what physics knows the economics doesn’t.

Why an income book has to behave differently from an investment book.

Can I lock in an acceptable annualized return and reduce my downside risk by 65-99%?

Read on you splendid thing!

Most options content sold to retail is really directional in disguise: selling puts or basic covered call writing is still essentially going long except the upside is capped. Effectively the way most options pundits purport to use tactics which don’t really reduce one’s risk but do cap their upside reward - in other words the opposite of the goal!

An income book has a different job. It has to produce cash flows and profits regardless of what the underlying markets decide to do in the meantime. That reframes the entire objective: the goal isn’t to be right about stock price direction. It’s to be paid for time and volatility while staying as indifferent as possible towards an assets price movement.

This piece examines: can a systematic options structure produce a real, competitive annual return while keeping price exposure (delta) near zero? Here I explain with real numbers on a real name — Agnico Eagle Mines (AEM).

Spoiler — the answer is yes, but requires an asterisk.

Options in three sentences, if you’ve never touched one

A call option gives someone the right to buy your stock at a set price (the “strike”) by a set date. If you sell a call against stock you own, you get paid up front (the “premium”) in exchange for capping your upside at that strike — you’re renting out your shares’ future gains. Everything below is just different ways of tuning how much you rent out, and managing overall exposure.

Why delta is the whole game

Delta measures how much a position moves per dollar the stock moves. 100 shares of stock is 100 deltas; that’s full participation, up and down. In an investment portfolio that’s fine. An income machine is a little different. I don’t want a down month in stocks to also be a bad month for my grocery budget. So the mandate becomes: collect premium, but manage the structure so directional risk stays small relative to the capital deployed.

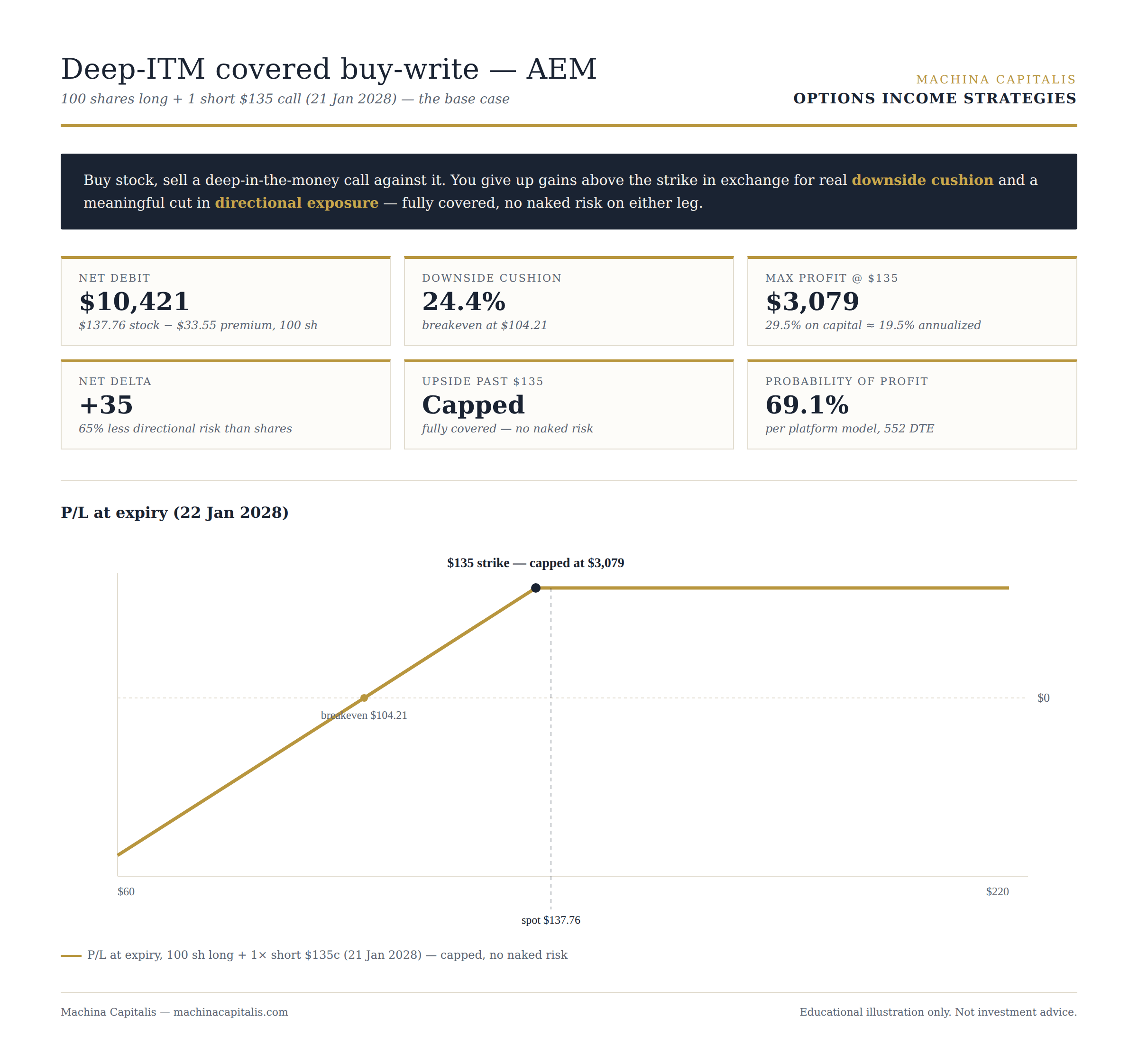

The base case: a deep-ITM covered buy-write

Take AEM, not a suggestion, just a random example for argument’s sake, trading at $137.76. Buy 100 shares (delta now 100), sell the 65 delta, a deep-in-the-money call (Jan 2028, $135 strike) against it for $33.55. That lowers the overall delta, or stock exposure to 35.

What does that do for me as a trader?

Net cost drops to $104.21/share — a 24.4% cushion before you’re underwater

Max profit is capped at $3,079 if the stock is called away, roughly 19.5% annualized

Net delta falls from 100 to about +35 — a 65% cut in directional exposure, just from selling one call

Upon entry, a 29.5% profit margin is secured while the initial working capital is protected. Less directional risk than owning the stock by itself, real income, real cushion. But let’s explore further possibilities.

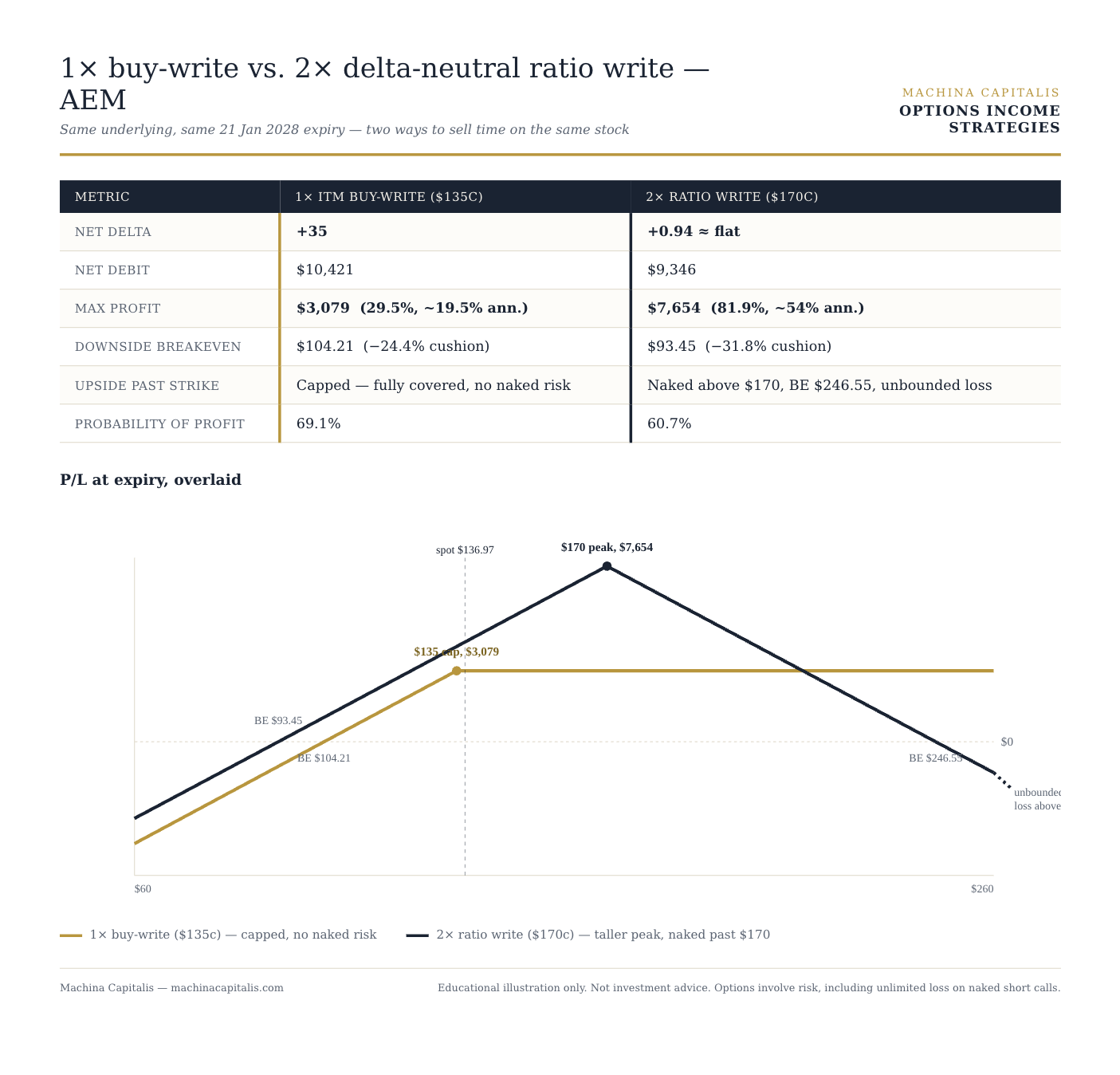

Turning the dial further: the ratio write

Let’s assume I wish to reduce my overall exposure from 35 above to 0 — or close enough. Here’s how I might do it; Go further out of the money and sell two 49-delta calls against the same 100 shares instead of one 65 delta call. Here something interesting happens to the delta math:

Long 100 shares (+100 delta) and short 2 x ~50 delta calls at the $170 strike for the same expiration date. Now my delta nets out to +0.94 — essentially flat

Downside cushion widens to 31.8% (breakeven $93.45, vs $104.21 on the single-call version)

Max profit more than doubles to $7,654 — ~54% annualized

The asterisk: One contract in that 2:1 ratio stays covered by the shares. The other doesn’t. Past $170, that second call is naked — the position caps out and starts losing money again above $246.55, with no ceiling on the loss. Near-zero delta today isn’t the same as staying near-zero over time: the “hedge” only holds inside a range.

Comparison

This is the trade-off in plain terms: more premium and a wider buffer, but more management is required as now the position is not fully covered and the trade will need to be monitored and adjusted to remain delta neutral to follow the price movements over time.

Circling back

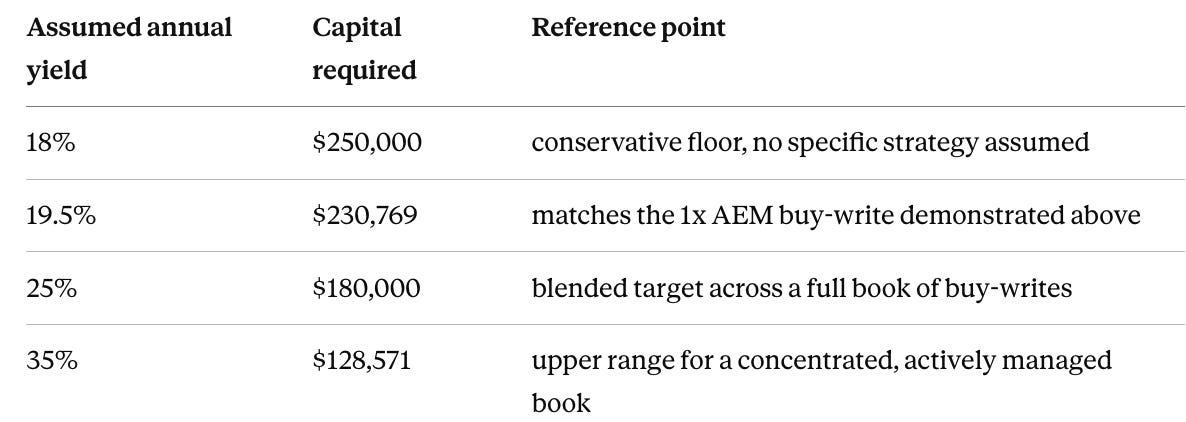

If a structure like this could realistically produce annualized returns in the high-teens (the mid 50% shown in the example would be preposterous to use as a base case for underwriting), while keeping delta near flat, the next question naturally is; how much capital does that actually take to replace an income?

Answered by simple arithmetic: Assume $45,000/year in expenses — a reasonable audited baseline for a modest, geographically flexible lifestyle. Here’s the capital required at a range of assumed yields, including the two we just walked through:

The honest version of this exercise isn’t “learn to do this and quit your day job”. It’s to gain awareness from exploring what’s possible and testable.

The Take Away - What’s The Point?

None of this is really about AEM. It’s about building an income source that doesn’t care where I am, doesn’t need a boss, doesn’t need employees, and doesn’t even need clients (at least none with whom I have to deal with directly). No physical inventory, no storefront, no team to manage, no fixed hours. The whole engine runs from a laptop and a brokerage account. For me, it’s been run in Mendoza, in Melbourne to Milan (to pchoose the M’s)

That’s really the product IMO: a business with none of the usual anchors. Cash flow that crosses borders alongside me, built on discipline instead of headcount.

If that’s the kind of independence you’re building toward, subscribe free — every week I break down one real structure like this, mechanics fully shown, so you can see exactly how the engine works, not just take my word for it.

Members get: Trades, Guidance, Performance updates and much more.

One for the comments: How interest are you in learning more about these types of systems?

All the best.

Benjamin

Machina Capitalis machinacapitalis.com · @TheRoyaltyKing