What's Your Freedom Number?

How much capital does it actually take to make a living from Options — the answer might be less than you think.

“ How much capital do I need to do this?”

This is by far the most common question I receive from readers who fancy building a borderless income stream of their own by running a one-man hedge fund, as I have. The answer to such a question is inherently personal and therefore necessarily nuanced, but nuanced does not mean unknowable. So today I am going to do something slightly unusual for this publication and write the answer as a recipe: from ingredients to step-by-step method along with a dash of my personal notes. By the end you will have your own number, and you will understand why each input belongs in the dish.

What’s on the Menu?

Freedom, fast-tracked.

Serves: One, adjust expenses according to number of people.

Preparation time: one afternoon

Cooking time: Varies with the individual, but years rather than decades for most readers.

Ingredients:

Your personal expenses - download all your bank statements and ask Claude et al. to calculate your monthly and annual expenditure (takes 5 mins).

One honest assessment of your skill level in generating investment returns (this ingredient cannot be substituted)

The formula: Freedom Number = Annual Expenses × Capital Multiple

A capital ladder (supplied below)

Optional: Re-location costs towards a more budget/tax friendly location

Optional (but recommended) A subscription to this publication

Method

Step 1 — Clarify The Core expenses

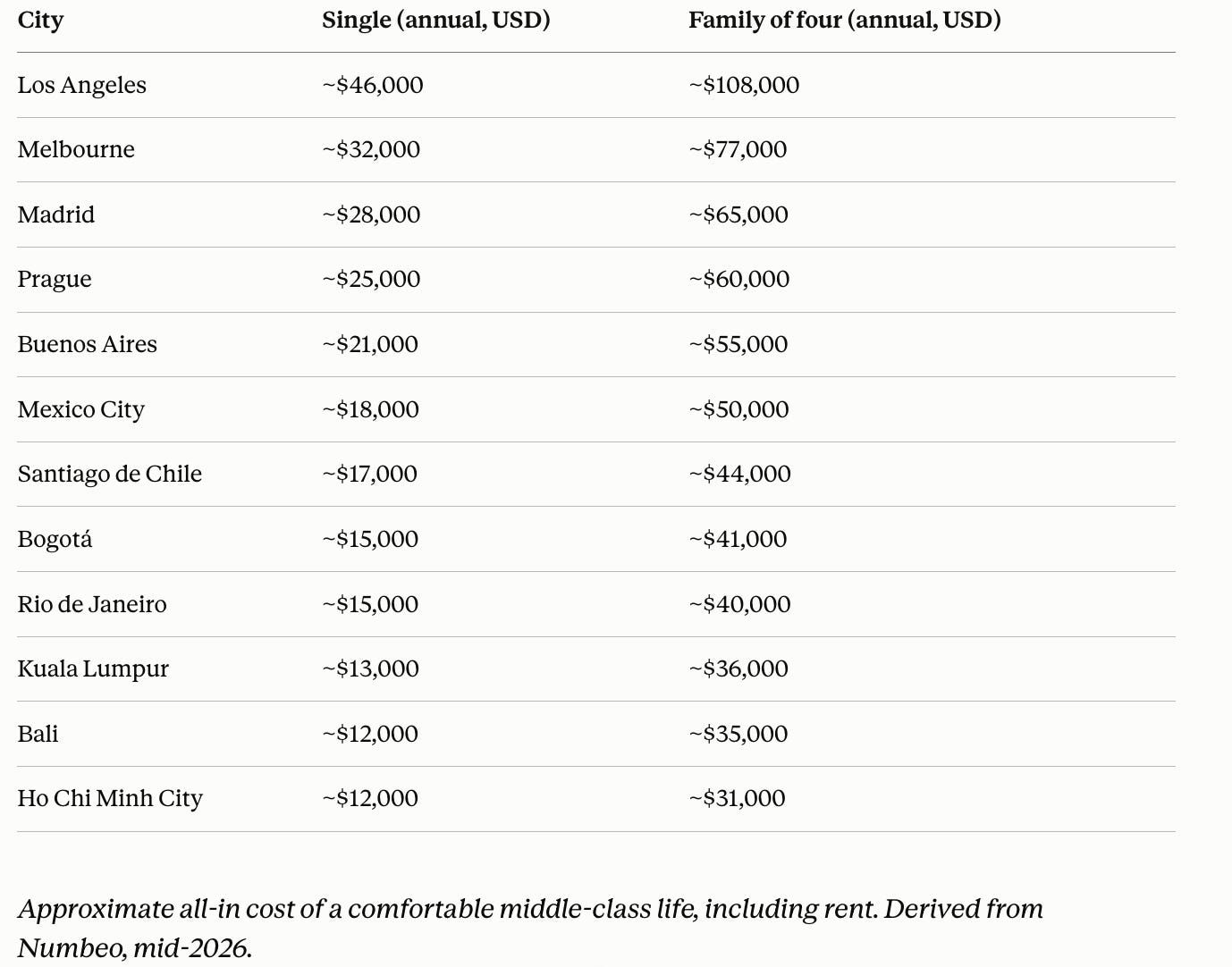

It’s key to distinguish between core (non-negotiable) and discretionary spending. For example, I have recently spent a lot of money on a trip to Italy - including a private tour of the Vatican etc - and all sorts of cool-but-expensive things. Obviously these are not core expenses. The key question to answer is how much is the non-negotiable cost of living for you and your family?

The mid-range estimate for the median annual cost of living in the USA is ~$25,000 for a single person to ~$60,000 per family.

Step 2 — Run The Formula

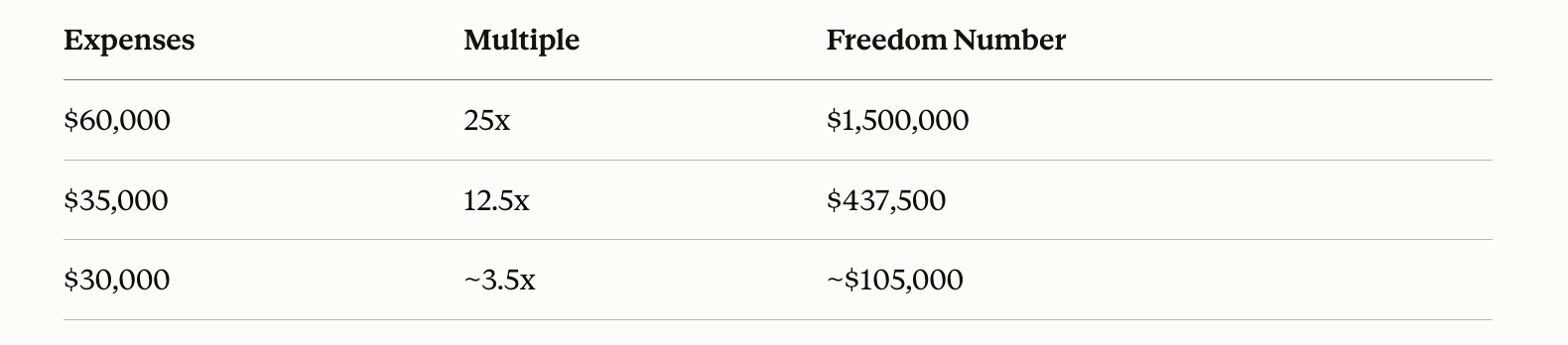

Freedom Number = Annual Expenses × Capital Multiple.

If we take that figure to a generic financial advisor they would reflexively apply the 4% withdrawal rule which assumes that in order to retire, the average portfolio can spend up to 4% of their savings per year and fund a retirement of ~30 years before the capital is all spent.

To calculate the capital required for one’s annual expenses above to equal a withdrawal of 4% simply calculate expenses by 25:

$25,000 × 25 = $625,000 for our single person.

$60,000 × 25 = $1,500,000 for the family.

Sit with that for a moment, because these numbers are disheartening for most. They require decades of diligent saving, a bull market that cooperates, and a retirement that arrives roughly on schedule with your pension — assuming one’s government has not changed the rules by that time. Of course there’s nothing wrong with this per se, but for my taste it’s completely unacceptable. It’s worth explaining that this rule was based on the 60:40 portfolios of the ‘80s and is only slated to last 30 years — I am in my 30s and don’t want to wait 20-30 years to enjoy independence.

Now look again at the formula.

Freedom Number = Annual Expenses × Capital Multiple.

Two variables. The industry treats both as constants yet neither is fixed. The rest of this recipe is the pulling of two levers and the discovery that when you can effect both of them, the barrier between you and your freedom shrinks non-linearly!

Step 3 — Adjust Lever 1: Expenses

For geographically flexible individuals, your expense number is more malleable than you think. A similar lifestyle: food, housing, internet , school fees etc — is priced differently in Melbourne than it is in Medellín (although I don’t recommend either). Reprice the core from Step 1 in a jurisdiction chosen deliberately rather than inherited, and you often find that 40–60% typically falls away.

In other words, the $60,000 PA family life might become $30,000–35,000 PA with less loss of luxury than one might expect.

Side note: If you earn in a hard currency and spend in a softer one, every tick of exchange-rate drift lowers your hurdle without you lifting a finger. My book is denominated in US dollars; my expenses are not. Expenses in the weak currency, income in the strong one — never the reverse.

Step 4 — Pull lever 2: Increasing returns

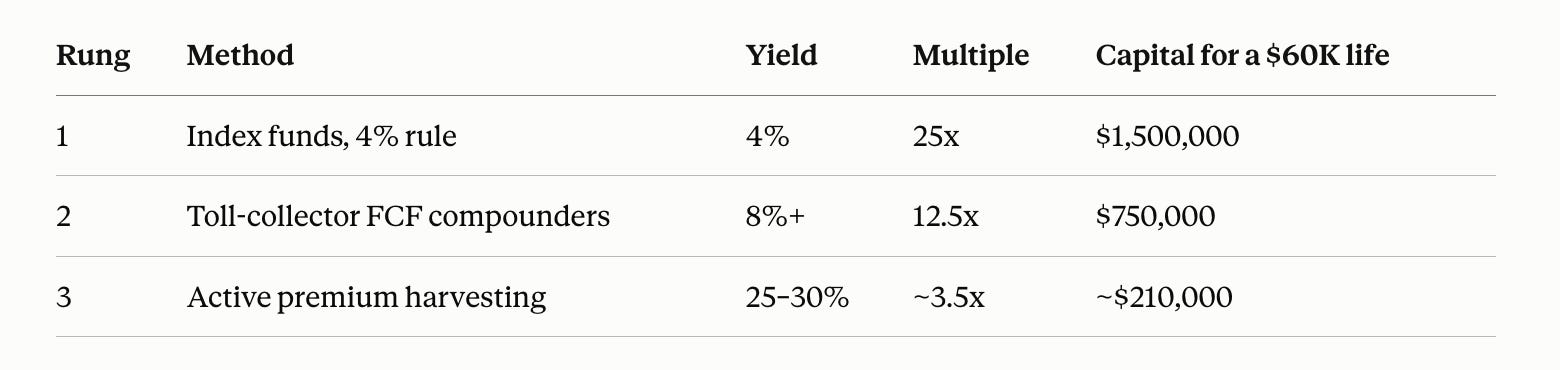

Climbing the capital ladder. And this takes work.

Above, we applied the standard rule of multiplying expenditure by 25. But ask yourself, why 25? Because 4% is the yield of someone who has effectively agreed, in advance, to know nothing. It represents the lowest historically reliable yield of institutional capital: index funds with no room for judgment, nor selection. It is the capital requirement of assumed ignorance. Arithmetically, the moment you upgrade your skills to improve on a 4% withdrawal rate, the required multiple falls precipitously. Let’s examine how improving one’s capital returns and by extension, permissible withdrawal rate, can drastically lower the initial starting capital required.

Rung 2 of the capital ladder represents ownership of superior businesses with inflation-protected free cash flow yields: the exchanges and royalties so often mentions in my other publication.

Rung 3 is the basic operating system documented in this publication, which stands today at 23.5% over 6.5 months — of course this is no guarantee of future performance etc etc.

Rung 3 is the most individually variable hence it is imperative that the reader apply an honest estimation of the returns they are able to generate with their individual skill set.

Step 5 — Multiply both levers

This is where the magic can happen thanks to an old friend — leverage.

Let’s run a hypothetical by pulling both levers simultaneously: reducing expenses and climbing up the capital ladder.

Potentially then, perhaps not the same lifestyle, but similar is theoretically possible with 50-90% less capital. Notice what the two levers do when pulled together: they multiply rather than add. The central point here is that with some intelligent design and the adoption of new ideas, one’s life can shift from coping to thriving.

Chef’s Notes:

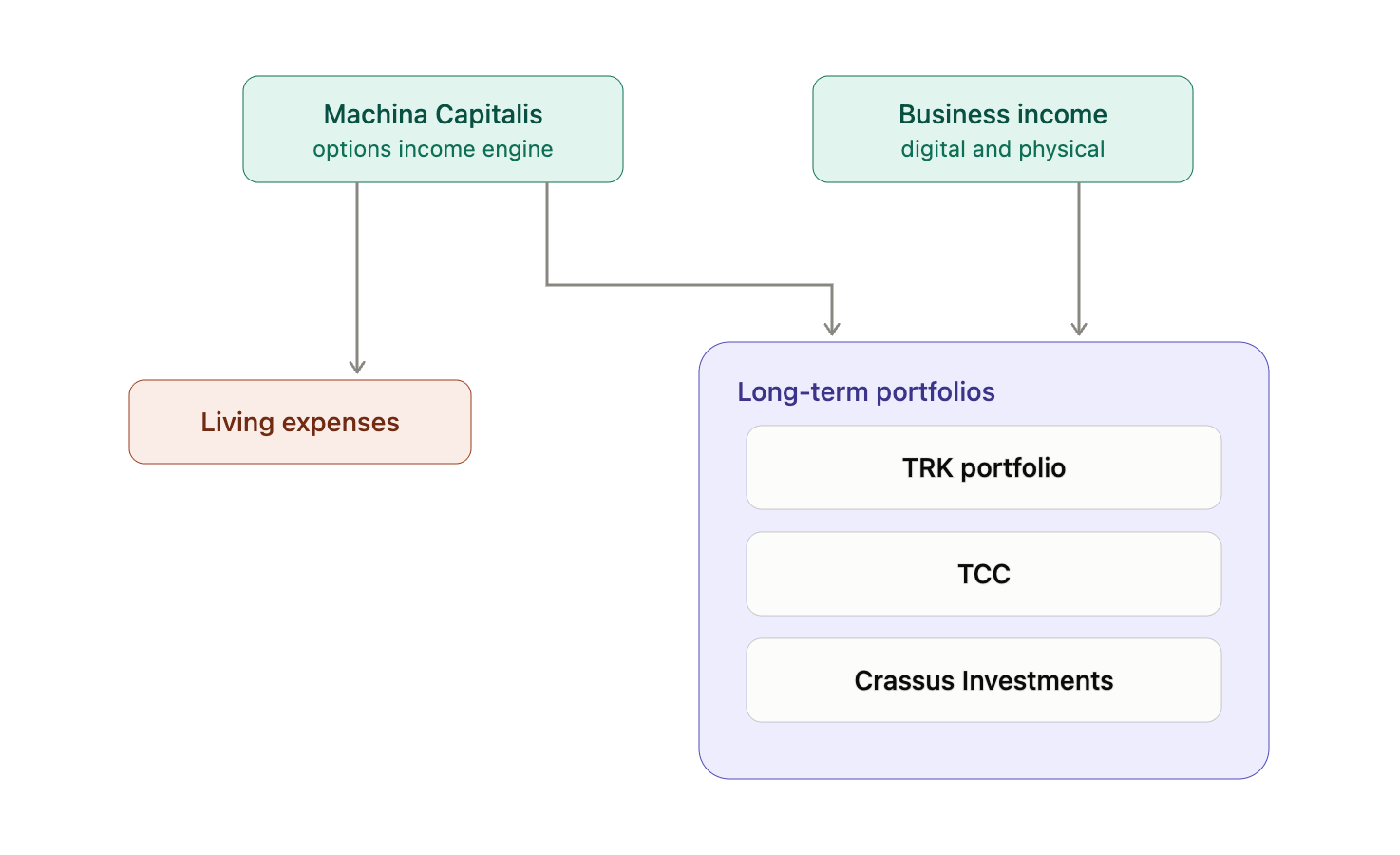

I began the year experimenting with $50,000 to seed Machina Capitalis and documenting the progress. Fairly quickly I was satisfied with the scalability of the project and determined that the optimal seed capital was ~$250,000 USD.

Why $250K? My personal expenses run about $45,000 US per year (ok you got me - I spend way too much, but it’s well covered by multiple income streams). I planned a range of ROIC (return on invested capital) of 18-30% ergo, calculating conservatively, the seed capital should be $45,000 ÷ 18% = $250,000.

In practice: I withdraw what I spend, not what I earn. The difference stays in the book as working capital — remember, this is an operating business not an investment portfolio. Once that surplus grows large enough, I move it across to my long-term portfolios. The fund pays for life; the long-term portfolios build wealth.

Important note: Taxes have been ignored here as each individual’s situation will differ, but none the less it should form part of year expense calculations.

All of this is less exotic than you might think - I merely suffer from exotic tastes!

An honest expense audit, a deliberately chosen location and a yield you can actually defend are the starting points. Run the recipe with your own figures this weekend and I suspect you will find what I found: freedom is not thirty years away. It is a design problem, and design problems have solutions.

I document mine in real time inside Machina Capitalis: every tactic, every trade and every month’s income — warts and all.

If you’d like to be a part of the group — subscribe today.

Until next time,

Benjamin.