I’m proud to be partnering with The Solstice Laboratory — At the cutting edge of Econo-physics.

Ray Dalio’s recent piece “Why I Recommend Being a Macro Long-Short Investor” caught my attention.

I liked the piece and, as much as I believe there’s way too much noise around “Macro” in the financial media, I can’t deny its importance on market capital flows and, by extension, my capital allocation.

Going long-short sounds simple and it does make sense, however it is difficult to apply practically for most individual investors. The reason being: it generally still involves essentially picking winners, only here the idea is applied relatively across companies, assets, sectors or even nations.

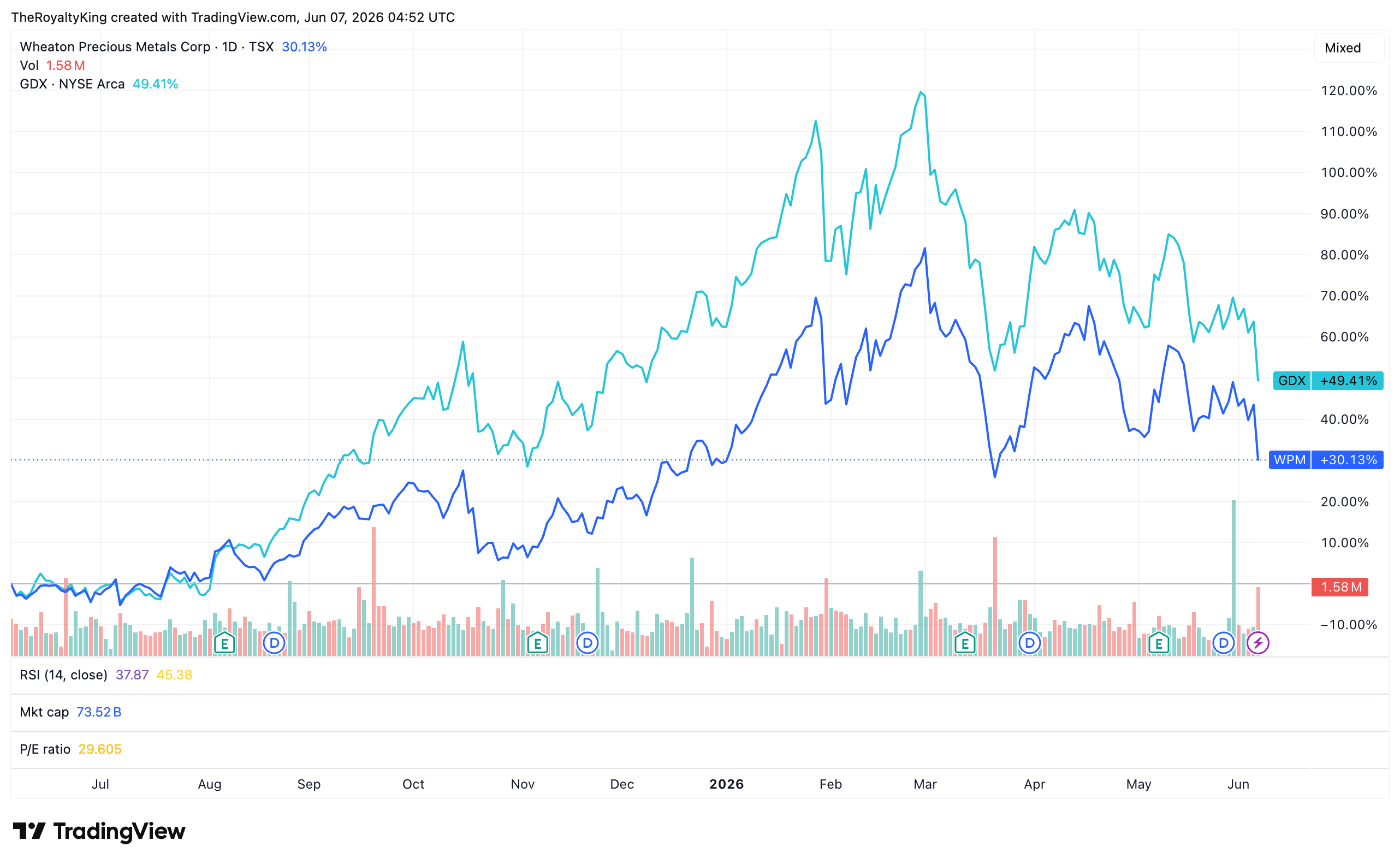

For instance: a popular trade idea over the last year has been long Brazil / short US stocks.

The trade performed well up until April, with EWZ up ~51% vs SPX ~16.5% for a net profit of 36% for a long-short trader.

Unfortunately however, the YTD performance now has reversed completely with a net performance of −2%.

Long-short Macro ergo isn’t really applicable to long-term investing for the mere mortals, as overstaying one’s welcome — even by only 2 months here — ended in a loss.

Traditionally, hedge funds targeted sector-specific long-short trades, being long the best in class + short the rest, or weaker companies. An example might include long WPM and short the GDX in the gold sector. Over a long-enough time horizon this particular trade has done well, and provided risk-adjusted outperformance during most gold markets, including Bear & Flat — highlighting the difference in underlying models.

Yet again, here a long-short investor needs to manage their timing, selection and leverage (Many hedge funds use copious leverage which is why they blew up all the time) because over the prior 12 months the quality has underperformed the broad index inside the very same sector by ~20%

This type of pair-trading or arbitrage is typical of long-short, and is why hedge funds were originally known as arbitrageurs.

So what if there was a way to utilise the power of long-short to achieve outsize risk-adjusted returns by going long-short on the same asset?

Enter Ed Thorp and the concept of warrant-hedging which I’ve adapted to call options.

The great Ed Thorp is one of my investing heroes and is a pioneer in quantitative finance — arriving on the scene well before Jim Simons et al — and is considered by many to be the true inventor of options pricing, formula known as the Black-Scholes formula. Ed released his work to Fischer Black and Myron Scholes (after having cleaned up in the derivatives markets for a few years prior).

The idea was to trade instruments on the same stock or asset in such a way to become market-neutral i.e. completely directionally agnostic as to price movement in the underlying and instead benefit from mis-pricing of the derivatives on the asset.

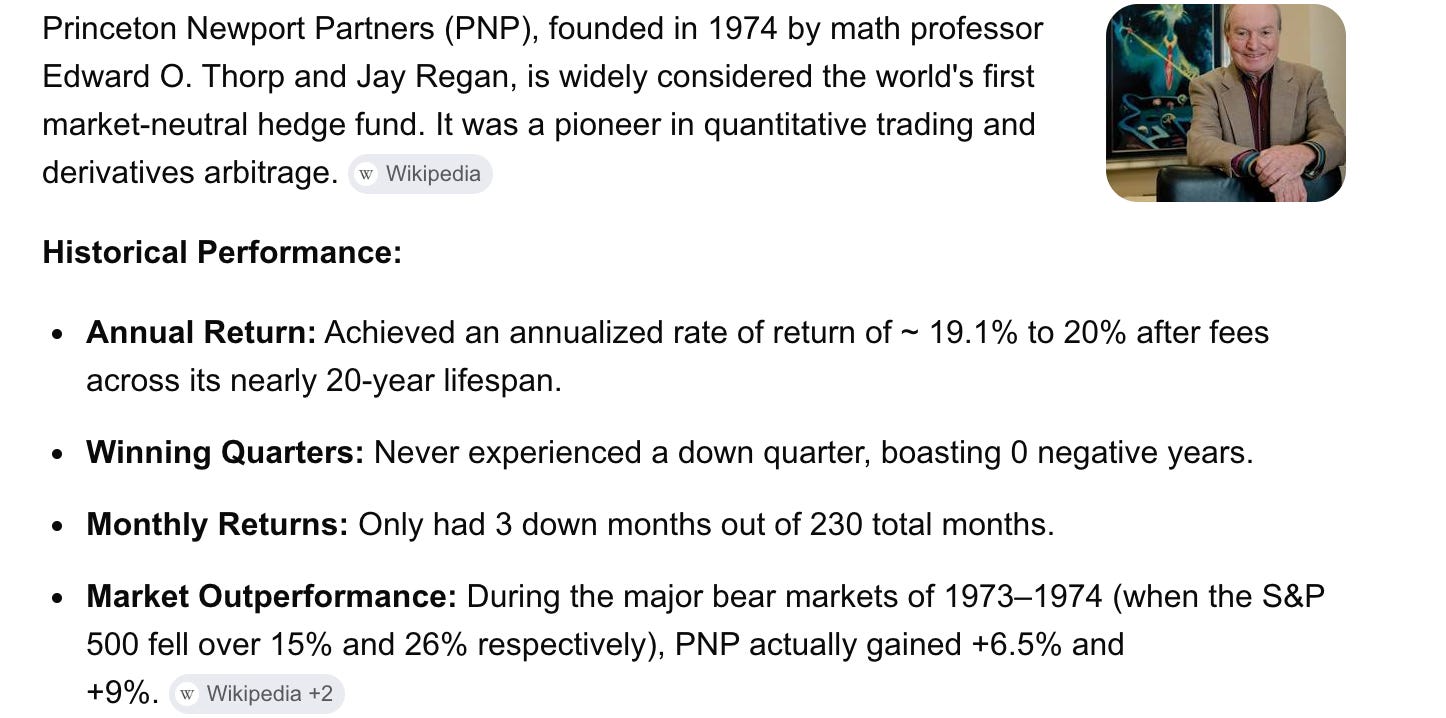

How well did this work? See for yourself.

This type of model has been on my mind a lot recently as today’s stock market volatility & geopolitical setup matches the ‘70s in many ways.

Given Machina Capitalis is a business for me — you might say it’s a 1-man hedge fund — the idea of making 20–30% annualized whilst significantly stripping directional price risk is highly attractive, and will more than suffice for my income needs without requiring a large amount of working capital.

How does it work — The Big Idea

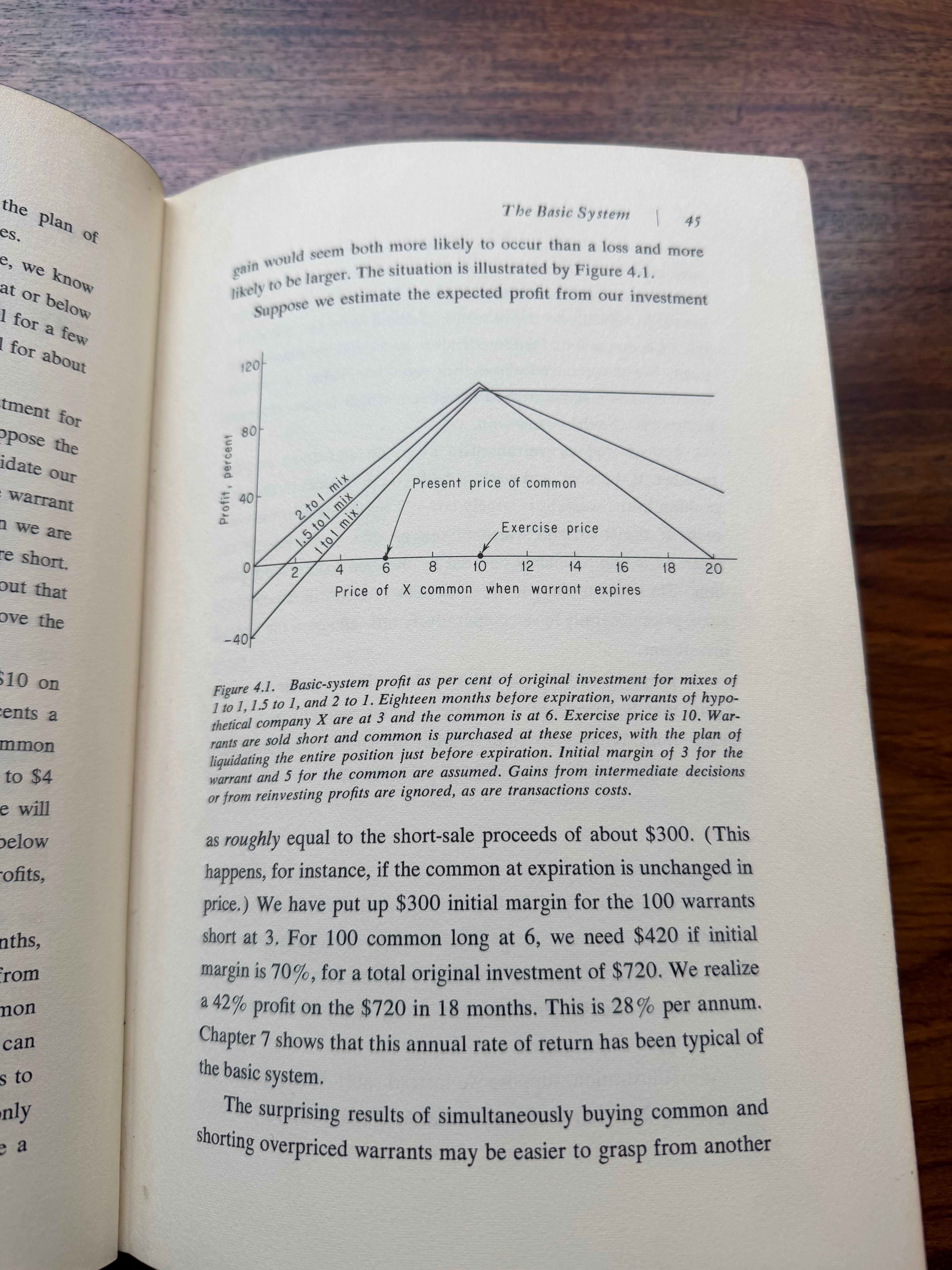

Simple. Ed used a basic system where he went long common stock and sold short convertible securities such as warrants that were overpriced.

He calculated the correct hedging ratio such that a net profit was expected by the expiration date of the warrants whether the price went up, down or sideways.

I’ve adapted this system here in Machina Capitalis by shorting call options to hedge in profits and/or significantly reduce the downside. Before you dismiss this as ‘just writing covered calls’ there are a few nuances to consider.

Factors such as: the strike placement of the short call, the ratio of long stock : short calls and how this can be adjusted over the life of the trade are — to my knowledge — available nowhere else.

Enough theory — let’s examine a real example of a trade I’m running right now.

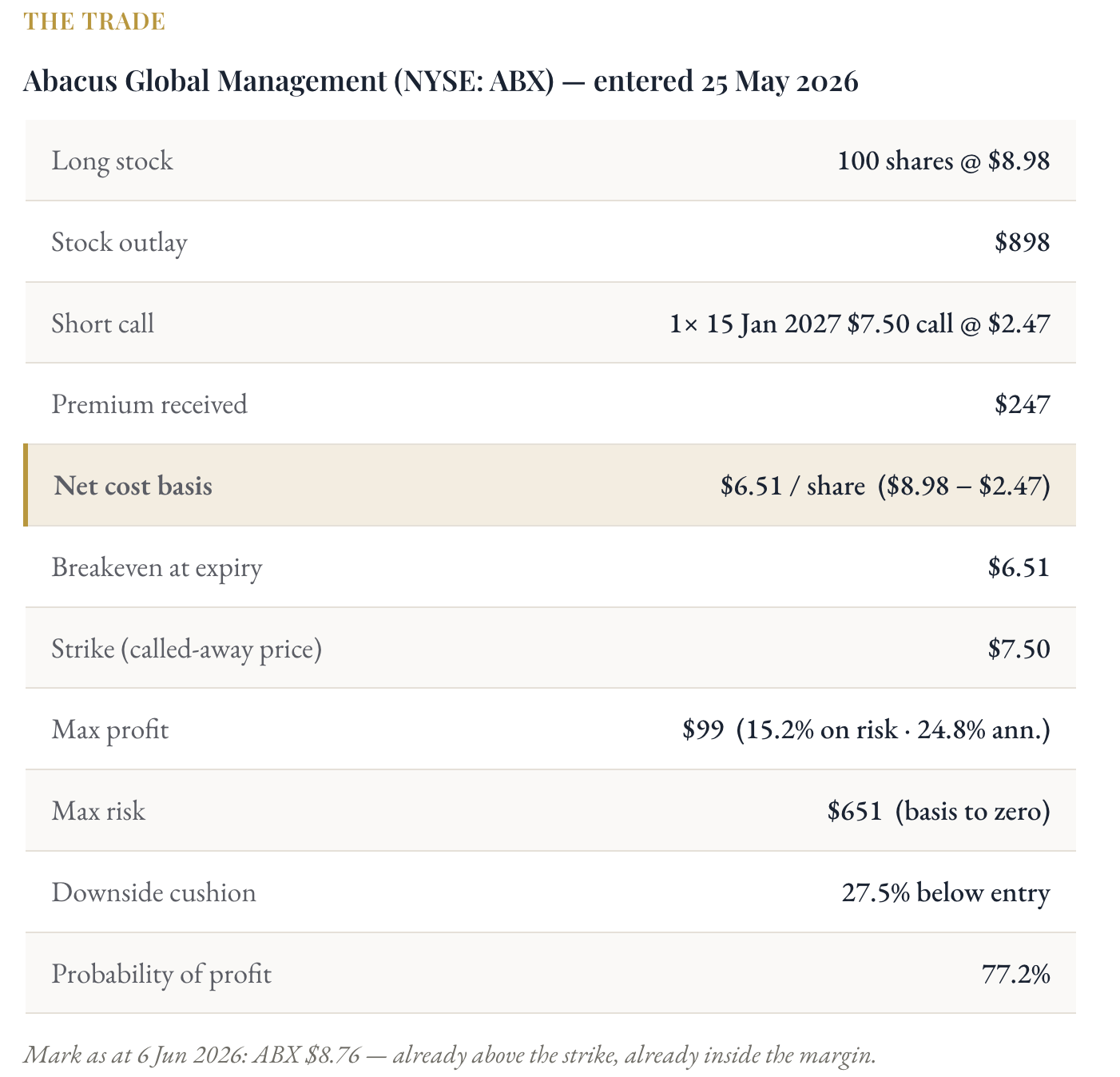

Hedged Trade: Abacus Global Management (ABX)

My book will not be run completely delta-neutral like Thorp’s was — meaning I’ll always have some exposure skewed directionally. This is because I don’t want to increase the management needs operationally — I want minimal running requirements + acceptable returns with significant downside protection. My edge is to stick to quality assets I know well; in addition to the quantitative factors, this should provide adequate risk-adjusted returns and so far has done so.

One tool I use frequently to get the best of all worlds is the deep-in-the-money covered call, meaning I buy an asset I like at a discount by simultaneously selling an ITM call option at a ratio of 1:1 (100 common = 1 call option).

ABX was trading at $8.98. I hold a positive long-term view on the stock as discussed with Unemployed Value Degen but want to hedge my downside here.

Therefore I executed a buy-write — buying 100 shares + selling 1 call option which expires in Jan ‘27. The trade looks as follows — my first tranche was to trade 15 lots.

The Hedge That Pays Me to Wait

Thorp and Kassouf considered a call option a short-term warrant. Sell one in the money against stock you own, and the basic system reappears — long the common, short the warrant, with a margin built in before the market moves at all. Effectively here’s what happened:

I paid $6.51 for a stock that redeems at $7.50. The ninety-nine-cent spread is locked in the day I put it on. 27.5% downside protection and a 24.8% annualized return on capital is guaranteed if ABX stays above $7.50 which has a probability of 77.2%. If I were so inclined, I could set, forget and check in in January. It pays to keep things simple.

Now let’s walk it through the potential outcomes.

Stock price falls below strike. This is the case the structure was designed for. From $8.98 down to $7.50 — a 16.5% decline — I still collect the full $99; the hedge has not even broken a sweat. Below $7.50 the call expires worthless and I am left holding the common, but at an effective $6.51, so I keep making money until $6.51 and only begin to bleed below there. And even then I am $247 better off at every price than the man who simply bought the stock unhedged. At $6.00 he is down $298; I am down $51. The premium is a constant $2.47-per-share head start that never leaves me.

Stock stays in range. Abacus sits at $8.76 today, already above my strike. If it simply refuses to move — drifts, churns, bores everyone — I am called away at $7.50 and book the full $99. This is the quiet feature of the in-the-money write: inertia is a winning outcome. I do not need the company to do anything. I need it not to collapse, and the market gives me that better than three times in four.

Stock rises more than 11%. Here is the opportunity cost. Everything above $7.50 belongs to the man on the other side of my call. So if Abacus climbs, my gain stops at $99 while the unhedged holder keeps going. The break-even between us is $9.97: below that I do at least as well as he does, above it he pulls ahead. To clear $9.97, Abacus has to rally 11% from where I bought in 6 months or so.

Of course it should be noted that I can always add to either the long or short side depending on price movement. Given call options tend towards zero as expiry approaches, I can adjust my ratio in a price slump by selling more calls at a higher price and buying more shares at a lower price and vice versa.

Adjusting the Ratio

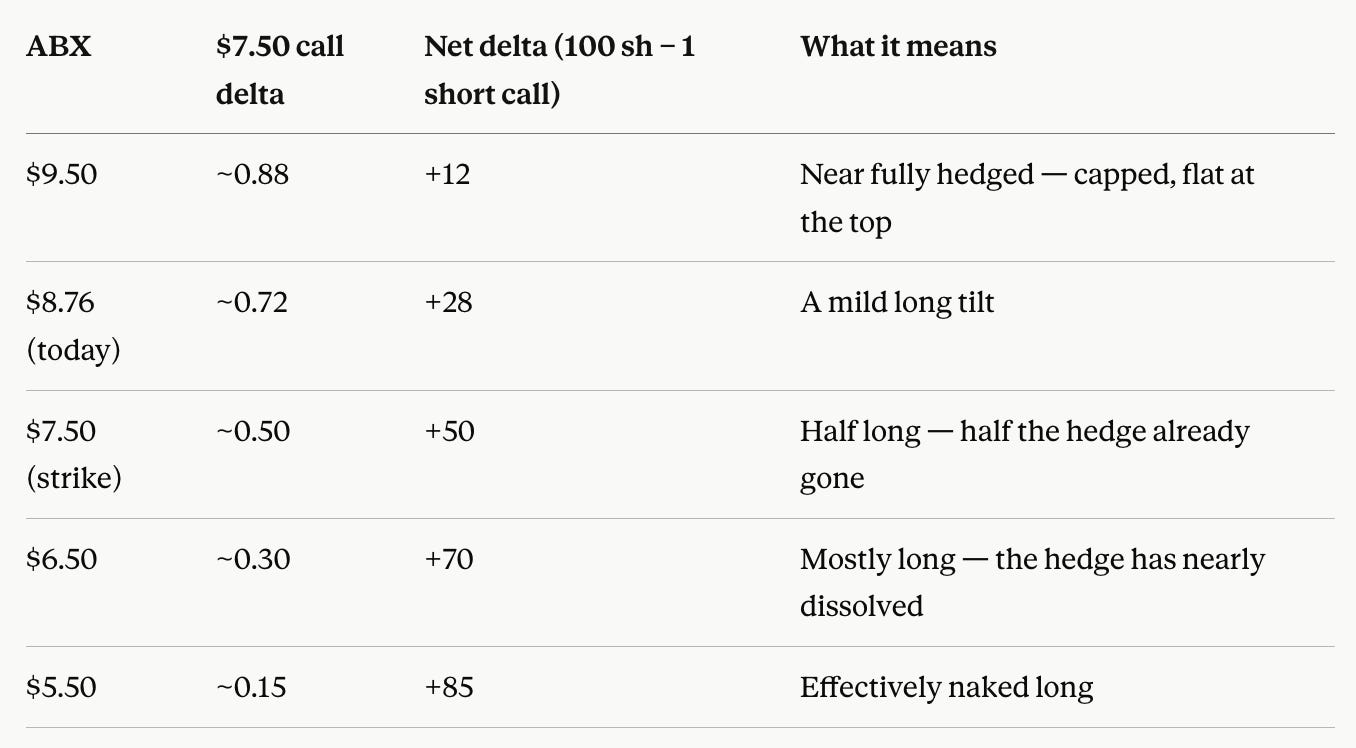

Ed Thorp never held a hedge still. The heart of the basic system was a ratio — so many shares long against so many warrants short — and the ratio was not a number he set once. It was a dial he turned as the stock moved, and the turning itself was where a good part of the money came from. He computed the ratio from the slope of his warrant-stock curve: how much the warrant moved for a dollar move in the common. We have a shorter word for that slope today. We call it delta. Ed was delta-hedging warrants by hand a decade before Black and Scholes gave the number its name.

A covered call has a mix too, and the first thing to understand is that it breathes on its own. My short call’s delta is the slope; my hundred shares are a fixed +100. The net of the two is the position’s true long exposure. I don’t have to adjust it, I can remain fully covered and relax, yet at times it may be worth adjusting.

Delta Table

As Abacus falls, my short call loses its delta, the hedge quietly lets go, and my P/L sensitivity gets longer and longer the common — not because I did anything, but because that is what a call's slope does as it goes out of the money. Most covered-call writers experience this as a problem as they are often stuck in the trade before they can re-write at the moeny, a more experienced trader might simply adjust the mix.

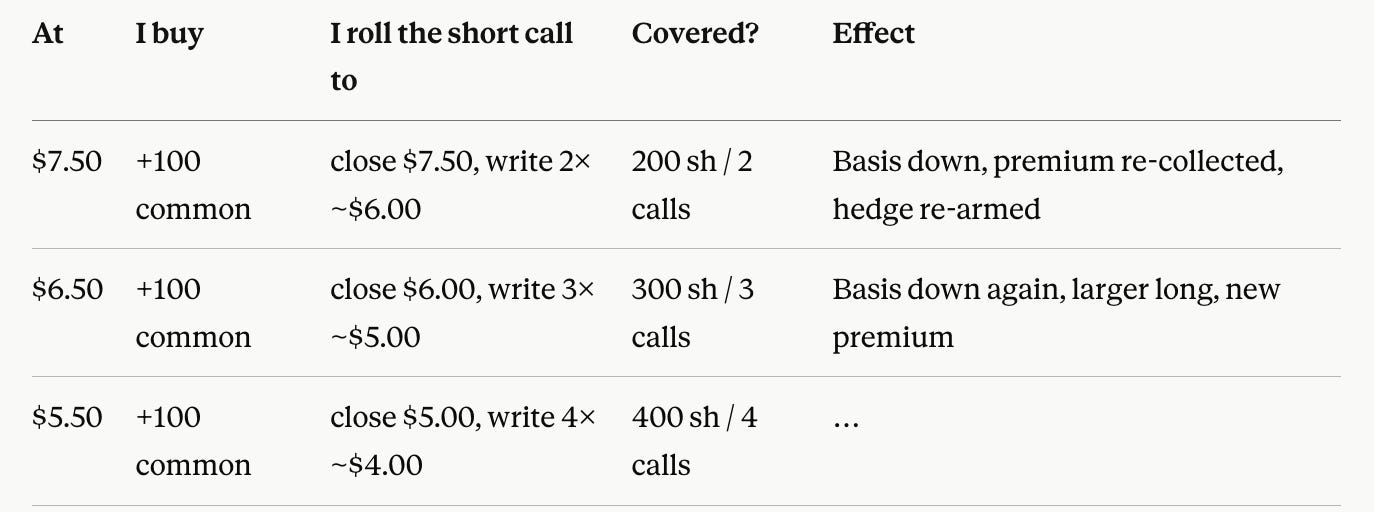

The down-ladder: changing the mix toward the long side.

When the stock falls through my strike, I do two things at once, and they are the same two things Ed did. I add to the long — buy more common at the lower price — and I re-arm the short by rolling (buying the original call now cheaper and re-selling) the call down to a lower strike, where its delta is high again and its premium is fat again. Each new hundred shares funds exactly one more covered call, so I am writing more calls as I descend, but never more than my shares cover.

What the ladder buys me, rung by rung is a lower blended cost basis and a hedge re-established at the new level instead of a dead one stranded up at $7.50. The breakeven walks down the price chart with me.

The up case is the easy one. If Abacus rises instead, the call’s delta climbs back toward 1, my net delta collapses toward zero, and the position caps itself — fully hedged at the top, exactly as designed.

Once again, I never allow my shorts to outnumber my longs, which would leave me exposed to a theoretically infinite loss in the event of a strong rally in the stock price.

I decide before I ever descend how many rungs I will fund and how large each may be, so that a continued decline depletes a planned allocation and never the entire book.

See my piece on the Kelly criterion.

Access My Entire Playbook

This is one position. Behind it sit several more using the same tactic and more still using more advanced tools

My method is portable by design. What I am building is a one-man hedge fund — borderless, digital, run from a laptop and a connection, owing nothing to a postcode. The same structure that pays me to wait on Abacus pays me from Mendoza or a café in Bologna, just as readily as from a desk in Melbourne. The income has no address. That is the freedom the system is actually for.

Premium members get the rest of it: every trade broken down the way this one was, the book updated live as I move it — each roll, each rung, each adjustment as it happens — and chat access to ask me directly. If today’s piece was useful to you, consider joining. And if nothing else, please like and share it — it’s the single biggest help in getting this work in front of the people who’d value it.

I’m leaning towards these ‘hands-off’ trades with 6-12 months expiry more and more recently - leaves more time to read, write and explore places like Puyehue, Chile in the above photo.

Next time I’ll be examining another popular options tactic— selling put options— and providing a post-mortem on some of my most recent, real-life trades.

Until then — all the best!

Benjamin.