In 1969, Ed Thorp began running what was arguably the first quantitative hedge fund. Princeton Newport Partners compounded 19% a year for 19 years — through the stagflation of the seventies and the crash of ‘87 — with zero losing years and only three down months out of 230. He did it by hedging mispriced warrants against common stock, collecting a spread that was locked in at entry. The market’s direction was, quite literally, someone else’s problem.

That system is the intellectual foundation of Machina Capitalis. I’ve adapted it to the modern options market, and in today’s video I show you the backbone of it: the deep-in-the-money buy-write, structured not for the yield-chasing you’ve seen a hundred times on YouTube, but for a locked-in spread with a downside cushion large enough to survive a market event.

The distinction matters, so let me be blunt about it. The popular version of the covered call: buy a stock you like, sell an out-of-the-money call “for income”, is a contradiction. It’s investing with the upside amputated. This is not that.

In my basic system the profit is calculated and locked at entry, the strike sits deep in the money, and assignment is a good outcome. If the profit calculator says no positive profit exists, the trade does not exist. Premium is the point; direction is someone else’s problem.

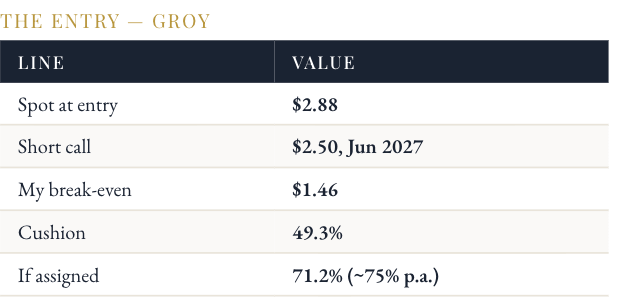

In the video I walk through a live example. Gold Royalty Corp (GROY) at a spot of $2.88, selling the June 2027 $2.50 call, for a break-even of $1.46. That is a 49% downside cushion. The stock can nearly halve before the position loses a dollar compared to a 71% return to expiry if assigned. Finding set-ups like that is most of the work.

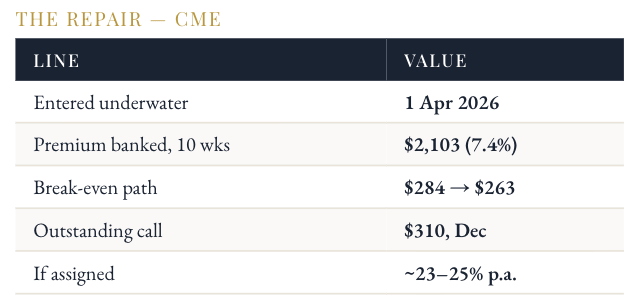

And because nobody should show only the trades that worked, that’s not what I do here in Machina, I also walk through one that went against me. My CME campaign entered on the 1st of April and promptly sank underwater. What followed is the actual product of this publication: ten weeks of selling calls against the position, banking $2,103 in premium — 7.4% of the position’s cost — and grinding the break-even down from $284 to $263. The position is repaired by cash flow, not by hope. That is what management looks like, and it’s the part that seperates a pro from a schmo.

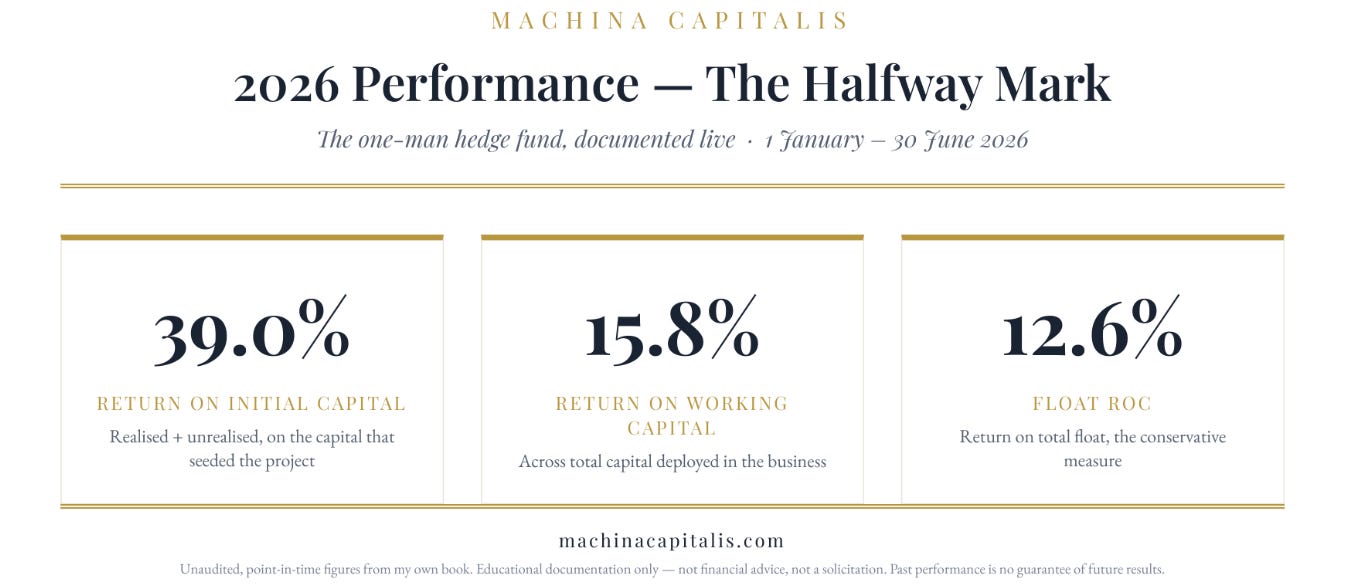

For premium members, the video continues into the full live book: the short path-dependent ETF overlay, the hedge decisions I made this week on QQQ, SPY and VIX, the ongoing TPL poor man’s covered call campaign — including some management I had to do to handle the trade’s volatility and my exact entry workflow from calculator to fill. In the next piece I’ll answer the question this entire project exists to answer: how much capital do you actually need to live off your capital alone?

At an 8% return versus a 25% one. The difference is not incremental. It changes what’s possible.

Machina Capitalis is educational documentation, not financial advice. Options involve significant risk of loss and are not suitable for all investors. Real positions are shown for transparency, not replication. Past performance is no guarantee of future results. Do your own research and consult a licensed adviser.