From Olive Presses to Options - Thales of Miletus & The First Options Trade In History

Options as vehicles for Speculation & Insurance

Long before spreadsheets or stochastic models, the first options trade was executed not by a banker, not even by a trader, but by a philosopher:

Thales Of Miletus.

Thales, a greek-speaking Ionian, lived in the 6th century BC in a little coastal trading post known as Miletus.

Aristotle recounts that Thales, like all philosophers of the time, was mocked for his lack of material wealth. “If philosophers are so wise,” critics said, “why are they poor?”

Thales answered not with words but with the following prowess: He paid cheap rental fees (read call options) to secure the rights to every olive press in the region for the upcoming season.

When the harvest arrived and demand exploded, those rights became extraordinarily valuable. Thales didn’t even need to press olives himself. He simply sold the now highly valuable rights for a massive profit.

He then went back to being a philosopher.

In modern terms, Thales had purchased a call option: the right, but not the obligation, to control a scarce asset. His downside was capped at the premium paid. His upside was open-ended. These trades exhibit extreme return-on-capital asymmetry in favorable outcomes.

By committing only a fraction of the capital required for ownership, one gains levered economic exposure without the fragility of debt or margin. These trades remain very much alive today and form a core pillar of Machina Capitalis as per the below example.

Insurance - The Other Side Of The Coin

Human societies have always tried to tame risk, a fact that lead to the invention of insurance.

Some of the earliest insurance contracts date back to Hammurabi of Babylon (modern day Iraq) in 1750 BC.

Hammurabi might be the first known underwriter of insurance by providing loss insurance on sea voyages within his kingdom. Put simply, if the ship returned successfully, the sailors repaid any loans + a fee (premium) whereas in the event of an accident, all loans were forgiven and the underwriter (Hammurabi) assumed ownership of whatever (if anything) could later be salvaged.

In modern parlance, Hammurabi effectively sold a put option.

This concept evolved over millennia into new forms such as the maritime insurance policies of Genoa and Venice in the 12-1400’s and the rise of Lloyd’s of London in the late 1600s. Insurance has always been about the same exchange: certainty for a price. Risk was transferred from merchants who could not bear loss to underwriters who could. That logic persists today. The seller of an option plays the role of the insurer absorbing uncertainty in exchange for premium.

In the case of Thales, the owners of the Olive presses gave away potential upside for the season in exchange for a guaranteed payment.

This forms the other side of the option coin: on one side, speculation, on the other insurance.

The advantage of the modern day options market is that it provides the savvy trader the opportunity to sell insurance on quality assets and effectively to get paid to wait for the opportunity to acquire them at a discount to current market prices.

(Example below).

Additionally there exists the ability to sell such options and then purchase cheaper ‘re-insurance options thus reducing the capital on hand required and hugely increasing returns on capital.

Both these tactics and many more like them form pillars of Machina Capitalis and membership gives access to specific ideas as to their implementation providing the opportunity for members to effectively form their own individual insurance company, a personal money machine.

Modern Day Markets

Exchange-traded options entered public markets in 1973 when the Chicago Board Options Exchange (CBOE) launched the first standardized, exchange-traded equity options.

For the first time, individuals could:

Sell insurance without being an institution

Rent out capital without owning factories

Fast-forward to today, with the expansion of the internet and technology, the Machina Capitalis documents the use of these tools to responsibly to generate income without inventory, staff, or geography

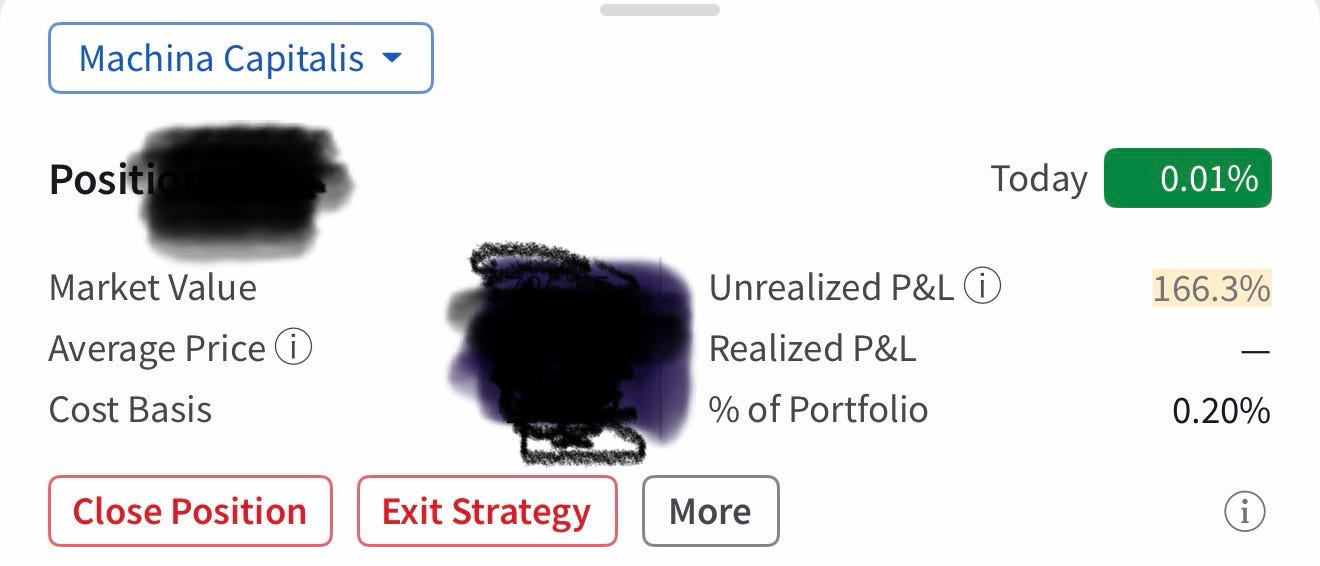

Like in this example: where I made $4,080 reserving just $43,920 capital over 40 days selling puts whilst on a road trip in remote northern Argentina.

Anywhere with internet access is fair game.

From Thales’ olive presses to Hammurabi’s trade loans, the purpose of the foregoing has been to establish a historical foundation for the concepts applied for profit within Machina Capitalis. While specific trades are provided, the deeper emphasis is on understanding the underlying architecture: how and why these tools work rather than simply distributing them. Mastery comes not merely from copying positions, but from grasping the logic that has governed risk, insurance, and asymmetric payoff structures for millennia.

If you’re interested in becoming a member and learning how I do this, please refer to the acceptance criteria on this page.

— Benjamin Demase

Founder, Machina Capitalis