Burford Capital: A Deep Value Speculation I Can’t Ignore

Special Situation Options | Hunting a potential 26x

Don’t forget to grab your ticket to the Rule Symposium below.

Machina Capitalis is my personal money machine.

Its purpose is to generate borderless income for me via: systematic options selling and, on occasion, high-conviction special situation speculations like the one I’m about to walk you through. Nothing here is financial advice.

These are my own positions, my own thinking, and my own risk which I document with members in real time. My skin is in the game.

Caveat lector!

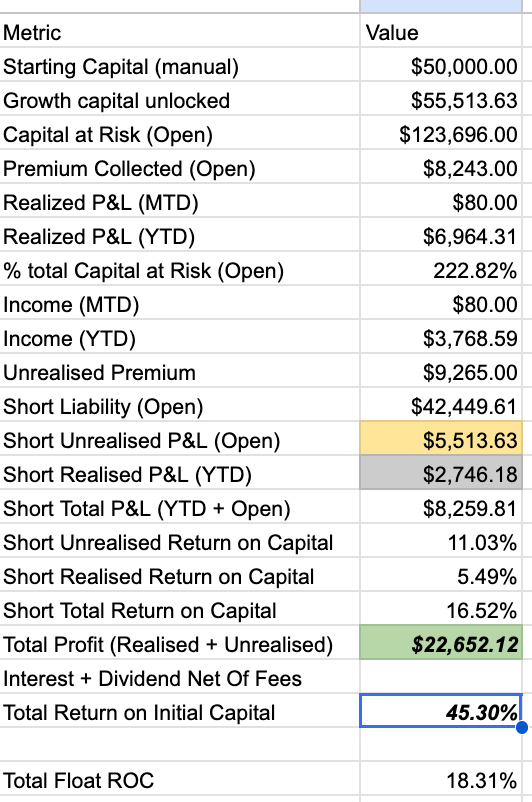

Performance

A brief update: Machina Capitalis is sitting at just under +45% total return on initial capital since inception (Jan 2026). I’m reasonably pleased. The goal is to deploy capital carefully and systematically where the expected value is genuinely compelling. This trade fits that brief.

Trade Setup: Burford Capital?

Let me be direct about something upfront: I don’t like this industry. Litigation finance is a business model I find distasteful.

That said, whether I like it or not, the business exists and it will continue to exist. Right now, IMHO the market is throwing the baby out with the bathwater and as a result the stock is trading at less than half its estimated book value. In these scenarios: betting on a reversion to book value and/or normalising market multiples, I’d rather own the options than the equity. I can collect the upside without having to be a long-term owner of something I find philosophically unappealing and it’s also much more capital efficient. That’s one of the genuine advantages of derivatives.

So what happened, and why does it matter?

The YPF Saga - Overreaction.

Burford had ashare of a ~$16 billion arbitration award against YPF, the Argentine state oil company (Yacimientos Petrolíferos Fiscales), in a case stemming from Argentina’s expropriation of the company. They won. Then they lost on appeal. Now they’re seeking a further hearing.

My view on the appeal: the probability of a meaningful recovery is low. Argentina defaulting on its obligations is practically a national sport at this point (I say that with affection as a ‘new Argie’). However, Burford is not going to extract $16 billion from a sovereign nation that has no real incentive to pay, where neither the US government nor any private entity is going to put geopolitical pressure on Buenos Aires over a litigation claim.

So I’ve written the YPF case to zero. That frees up my mental energy to ask a much more interesting question: what is this company worth without the case?

The Underlying Business

Strip out the YPF noise and you have a business case:

Book value of ~$5.2 billion, modeled internally by Burford without the YPF award

Low correlation to markets; litigation outcomes don’t care about the S&P or Fed rate decisions

Lumpy but high-quality cash flows. Suits resolve on their own timeline, not quarterly earnings cycles

Historically valued at 1.5x–2.5x book suggesting intrinsic business quality that the market has recognized before

At the time of writing, the stock is hovering around $4.50, giving a market cap of roughly $1 billion against that $5.2 billion book. I’d be buying the business at less than 20 cents on the dollar of stated asset value and that’s after writing the big case to zero.

My base case is a reversion to 1x price-to-book within two years and implies a target of $11–$12 ex growth assumptions. A bull case, where the market awards a more typical 1.5x–2x multiple and book value compounds modestly in the interim, takes the price toward $18–$20.

On the equity alone, that’s a 3-bagger at base and a 5-bagger or more at bull. But I don’t want the equity. I want the options.

Because the logic is; If the thesis is right, why not maximise upside with minimal capital?

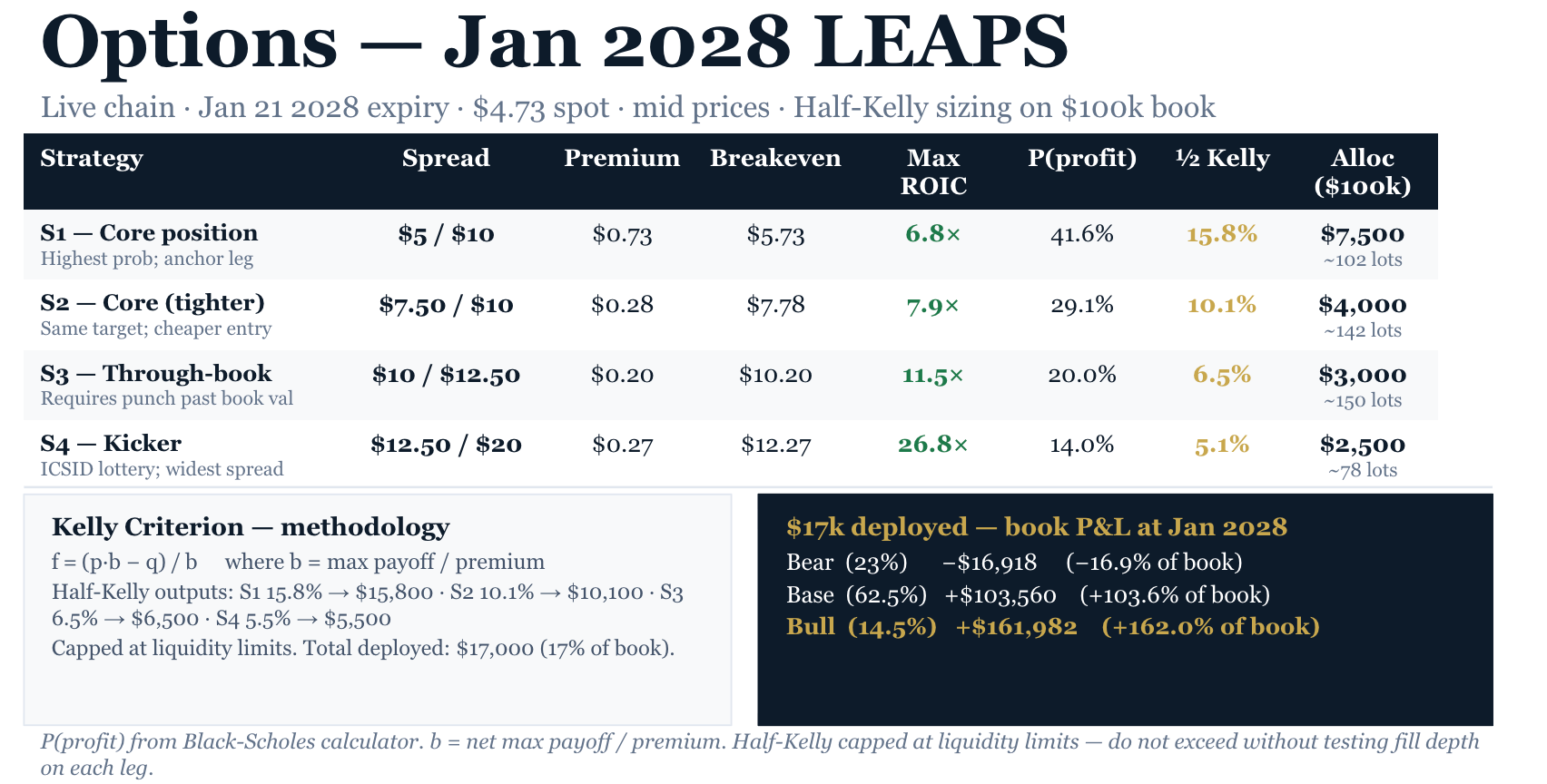

The Options Structure: January 2028 LEAPS: Bull Call Spreads

Because this is a binary-ish situation with a multi-year timeline, I’m using January 2028 LEAPS giving me approximately 21 months of runway. In my experience, special situations and re-ratings always take longer than you expect. Time is the engine. Theta is the enemy. So I look further into the future when express a long-side speculation while the inverse is true when selling options (on the short side).

The structure is a bull call spread: buy a call at one strike, sell a call further out of the money. This does two things; it reduces my net premium paid (by capturing the premium on the short call) and it caps my upside at the short strike, which I’m fine with because I’ve set my strikes at levels consistent with my base and bull case targets.

I’m running four different spreads across the options chain: a high-probability, lower-payout spread (breakeven just above current price) to more aggressive spreads targeting $12.50-20. Each is sized differently. This chain is fairly illiquid and I’m using the mid-price between bid-ask, putting buy orders in on the long leg first. I plan to sell the OTM calls (the short leg) as the underlying stock price rises (assuming it does) which effectively means I have even higher potential pay offs than stated with less capital in the trade.

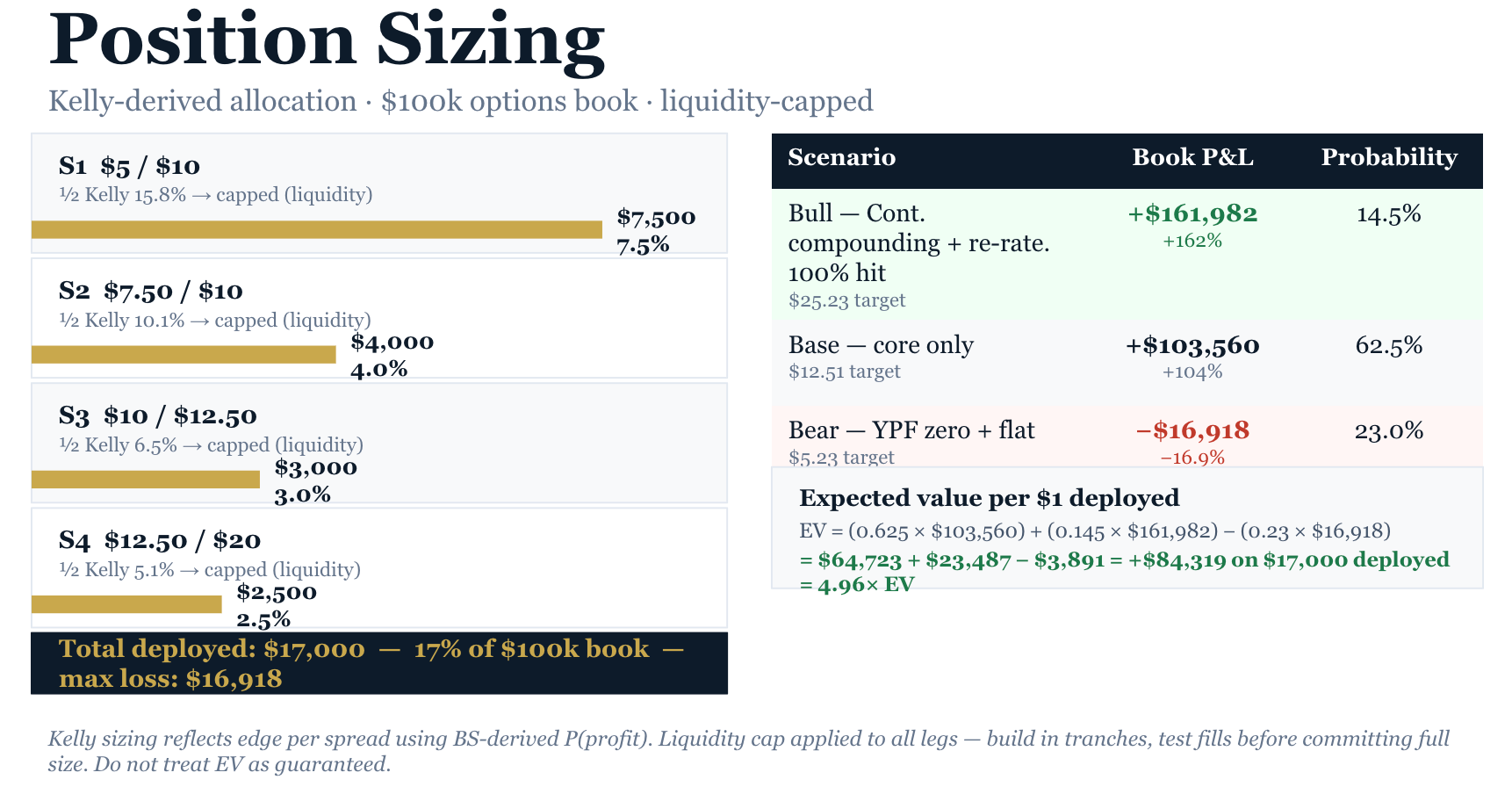

Position Sizing: Kelly and Half-Kelly

I’m running a separate sub-book purely for these special situation speculations. For position sizing, I use the Kelly Criterion, or more conservatively, half-Kelly to optimally size each bet based on probability of success and payout ratio. This keeps me from over-concentrating in any position and ensures that even if I’m wrong on the direction, the losses are survivable.

Total capital at risk across all four spreads: ~$17,000 — assuming all my orders get hit. As of today some have, not all.

Expected Value Summary

Running the numbers across bear, base, and bull cases:

Aggregating probability-weighted payoffs across scenarios, the expected value on capital deployed is approximately 5x and that is using an estimated 23% probability of a complete loss, that is, the stock price goes nowhere or down over the next 645 days - which seems an overestimation to me, but I won’t argue with the computer.

It needs to be understood that the EV is not a guarantee — it’s a mathematical output of probability estimates, which are of course subjective. But it gives you a sense of why the thinking behind the trade.

Base case outcome on total book: ~100% return on the full $100k using less than a fifth of it.

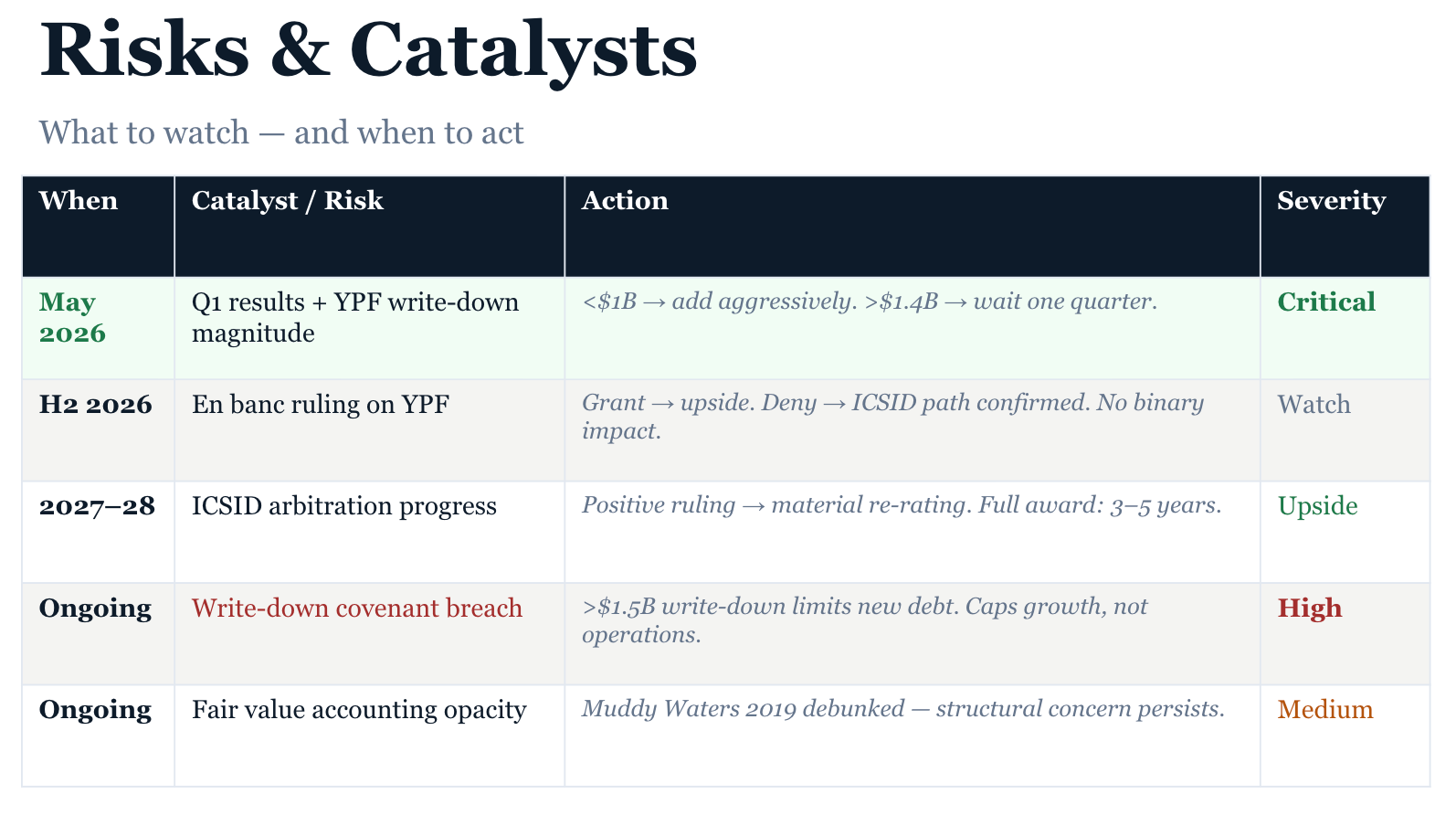

The short-term price action will likely be driven by headlines, and there are a few worth monitoring:

YPF appeal developments — I assign near-zero probability to a recovery, but the headlines will move the stock either way

Quarterly earnings (MAY) and book value growth — any evidence the core portfolio is compounding is a positive catalyst

Broader risk-off rotation — if markets become volatile and investors seek uncorrelated alpha, a business with no macro sensitivity starts to look quite attractive

There remains the risk of an improbable string of case losses

Accounting opacity; Internal models are done by BUR. How trustworthy are a bunch of lawyers?

The Bottom Line

A ~$1 billion market cap company sitting on $5.2 billion in estimated book value, with a core litigation finance business that has historically earned 1.5x–2.5x book multiples, in a post-event selloff driven by a binary case I’ve already written to zero.

I don’t want to own the equity. But I’m very happy to own leveraged control over the stock via the options.

Become A Member - Special Offer

If this is the kind of thinking you want access to: special situations, options structures, income plays, and the full position-level transparency, Machina Capitalis is where it’s shared. My birthday is April 21, so I'm running 20% off special offer to celebrate. Use the code below for 20% off your membership forever.

https://www.machinacapitalis.com/23f1c11f

All the best,

Benjamin.

Position initiated: 16 April 2026.

The content published in Machina Capitalis is for informational and entertainment purposes only. Nothing contained herein constitutes financial, investment, legal, or tax advice. All positions and trades discussed reflect the author's personal portfolio and opinions at the time of writing. Past performance is not indicative of future results. Options trading involves significant risk of loss, including the potential loss of the entire amount invested. You should always conduct your own independent research and consult a licensed financial adviser before making any investment decision. The author may hold positions in any securities mentioned at the time of publication.